The American First-Time Homebuyer Tax Credit Act

The Issue

Executive Summary

This proposal establishes a targeted, regionally adjusted federal tax credit of up to $50,000 for eligible first-time homebuyers. The credit is designed to increase homeownership, reduce generational wealth gaps, and stabilize housing markets, all while remaining fiscally responsible, capped at $37.5 billion per year, equivalent to the current ICE annual budget.

Background & Rationale

Homeownership remains the primary means of building intergenerational wealth in America. Yet, as of 2024:

· The average age of a first-time buyer hit an all-time high of 36.

· Black, Latino, and low-income families face increasing barriers to entry.

· Rising interest rates and limited housing stock have priced many out of the market entirely.

Meanwhile, existing federal support is either outdated or insufficient. This targeted tax credit offers a direct and modern solution.

Policy Proposal

Core Components:

1. Up to $50,000 tax credit for first-time homebuyers.

2. Regionally adjusted credit tiers to reflect local housing markets.

3. Income-based phase-outs to ensure funds go to those most in need.

4. Home price caps by ZIP code based on HUD and Fannie Mae guidelines.

5. Split disbursement: $25K at closing; $25K spread over five years.

6. Residency requirement: Must live in the home for 5 years to retain full credit.

7. Annual budget cap: $37.5 billion/year.

Fiscal Plan

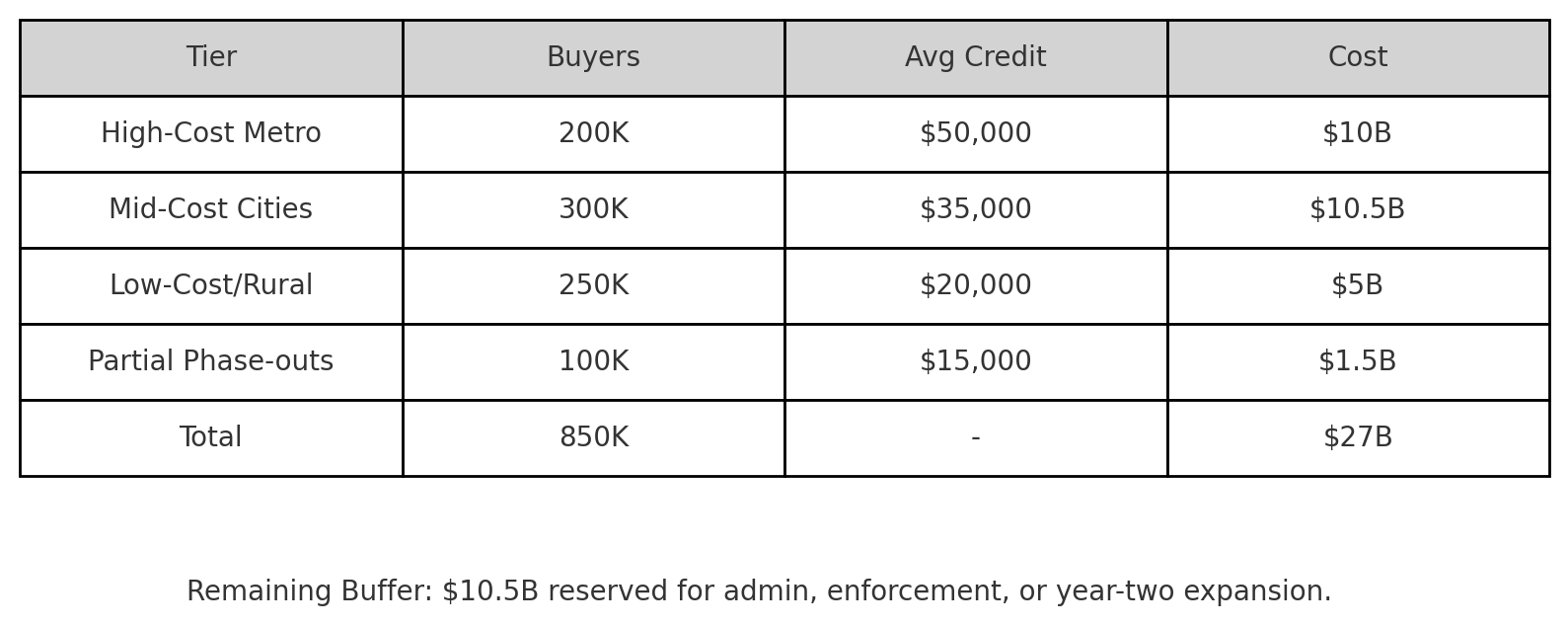

Estimated Participation (Year One):

Benefits

- Equity: Narrows racial and generational wealth gaps.

- Flexibility: Allows regional variation without penalizing rural or low-cost areas.

- Growth: Boosts construction, retail, and local tax bases.

- Affordability: Keeps housing prices stable by limiting oversubsidization.

- Accountability: Annual cap ensures budget discipline.

Legislative Simplicity

This plan:

- Can be introduced as a standalone bill or as a housing amendment to an appropriations package.

- Leverages existing IRS infrastructure for distribution and verification.

- Builds on historical precedent (e.g., 2008–2010 first-time buyer credits).

- Requires no new agency—can operate under Treasury and HUD.

Conclusion

The American First-Time Homebuyer Tax Credit Act provides bold, equitable action on the housing crisis without expanding federal bureaucracy or overspending. Reallocating existing budgetary priorities—such as ICE's $37.5B budget—would allow the program to launch without new taxes or added deficits.

It’s a fiscally sound investment in American families, workers, and communities.

10

The Issue

Executive Summary

This proposal establishes a targeted, regionally adjusted federal tax credit of up to $50,000 for eligible first-time homebuyers. The credit is designed to increase homeownership, reduce generational wealth gaps, and stabilize housing markets, all while remaining fiscally responsible, capped at $37.5 billion per year, equivalent to the current ICE annual budget.

Background & Rationale

Homeownership remains the primary means of building intergenerational wealth in America. Yet, as of 2024:

· The average age of a first-time buyer hit an all-time high of 36.

· Black, Latino, and low-income families face increasing barriers to entry.

· Rising interest rates and limited housing stock have priced many out of the market entirely.

Meanwhile, existing federal support is either outdated or insufficient. This targeted tax credit offers a direct and modern solution.

Policy Proposal

Core Components:

1. Up to $50,000 tax credit for first-time homebuyers.

2. Regionally adjusted credit tiers to reflect local housing markets.

3. Income-based phase-outs to ensure funds go to those most in need.

4. Home price caps by ZIP code based on HUD and Fannie Mae guidelines.

5. Split disbursement: $25K at closing; $25K spread over five years.

6. Residency requirement: Must live in the home for 5 years to retain full credit.

7. Annual budget cap: $37.5 billion/year.

Fiscal Plan

Estimated Participation (Year One):

Benefits

- Equity: Narrows racial and generational wealth gaps.

- Flexibility: Allows regional variation without penalizing rural or low-cost areas.

- Growth: Boosts construction, retail, and local tax bases.

- Affordability: Keeps housing prices stable by limiting oversubsidization.

- Accountability: Annual cap ensures budget discipline.

Legislative Simplicity

This plan:

- Can be introduced as a standalone bill or as a housing amendment to an appropriations package.

- Leverages existing IRS infrastructure for distribution and verification.

- Builds on historical precedent (e.g., 2008–2010 first-time buyer credits).

- Requires no new agency—can operate under Treasury and HUD.

Conclusion

The American First-Time Homebuyer Tax Credit Act provides bold, equitable action on the housing crisis without expanding federal bureaucracy or overspending. Reallocating existing budgetary priorities—such as ICE's $37.5B budget—would allow the program to launch without new taxes or added deficits.

It’s a fiscally sound investment in American families, workers, and communities.

The Decision Makers

Petition Updates

Share this petition

Petition created on July 9, 2025