Repeal Georgia’s Mandatory Auto Insurance – End the Mandate, Lower Costs for Law-Abiding

Repeal Georgia’s Mandatory Auto Insurance – End the Mandate, Lower Costs for Law-Abiding

The Issue

>when you sign the petition check your Gmail to confirm that you meant to sign it.

Proposal: Repeal Mandatory Auto Insurance Requirement (O.C.G.A. § 40-6-10) to Reduce Costs for Georgia Drivers

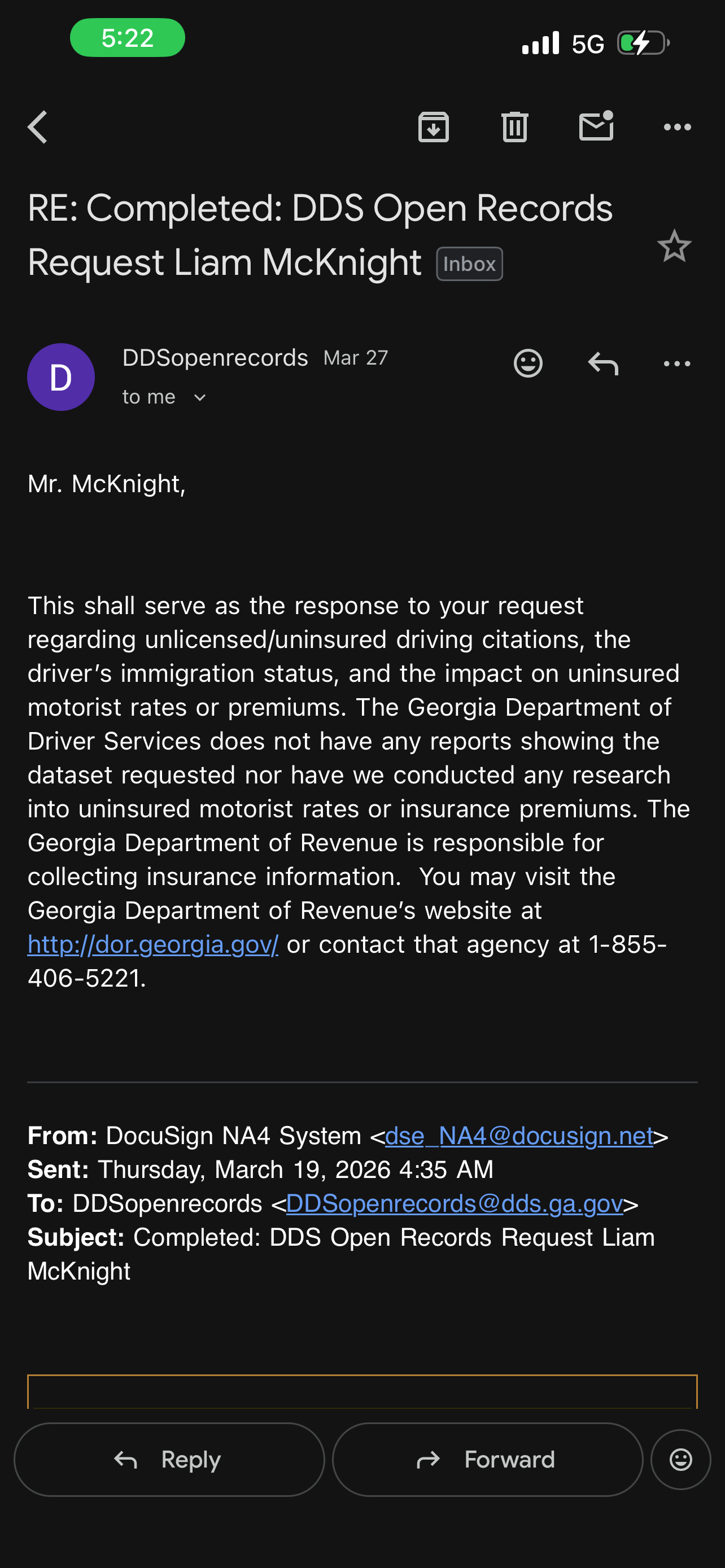

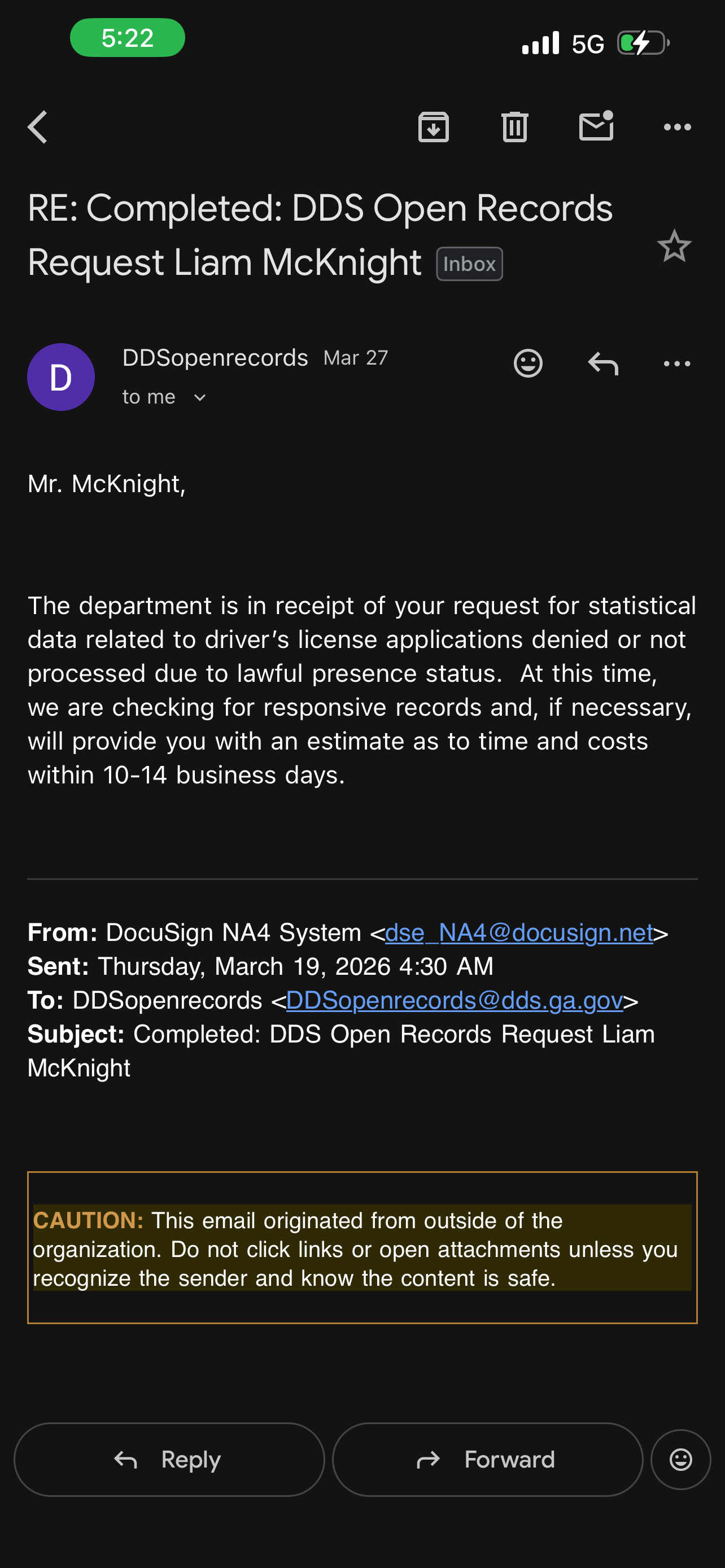

Hello Team,

Pathos/

haven’t you heard?

https://m.youtube.com/watch?v=97W_mgA8Ytg

I live at - in both Fulton and dekalb. My grandfather was the dean of Emory’s Goizueta Business School in the 60s, and I am a graduate of Oxford12 and GBS14 with concentrations in marketing and information systems. Read Machine Platform Crowd & The Master Switch: Information Empires & Big Data (2013) by Viktor Meyer Schunberger and Kenneth Cukier (this one is key to chekovs gun firing when you need it to and not only against you because of not data silos either your own or a company’s). I invented the over-the-shoulder cellphone holder in 2021.H2 to put any competent courier in the top .01% of current instacart couriers and top .00001% of all other shopper crowds on other delivery apps. This is crucial because AI wants your body, not your mind, and it a priority that we disintermediate these platforms who do not want to empower their employees because they would rather charge more for worse service (eg charging for faster service and just slowing down the normal tier of service) and making their entire shopper crowd superhuman would crush their existing business model because there is not enough work to be done because there are no incentives to use couriers and receive calls in broken English about whether you want whole or 2% milk replacement when desperately poor people are afraid to use their own discernment because of their precarious roles in the gig economy — whereas I was a rich courier who would have other couriers deliver to my Sausalito residence while I was making the money and keeping people happy with what they want./

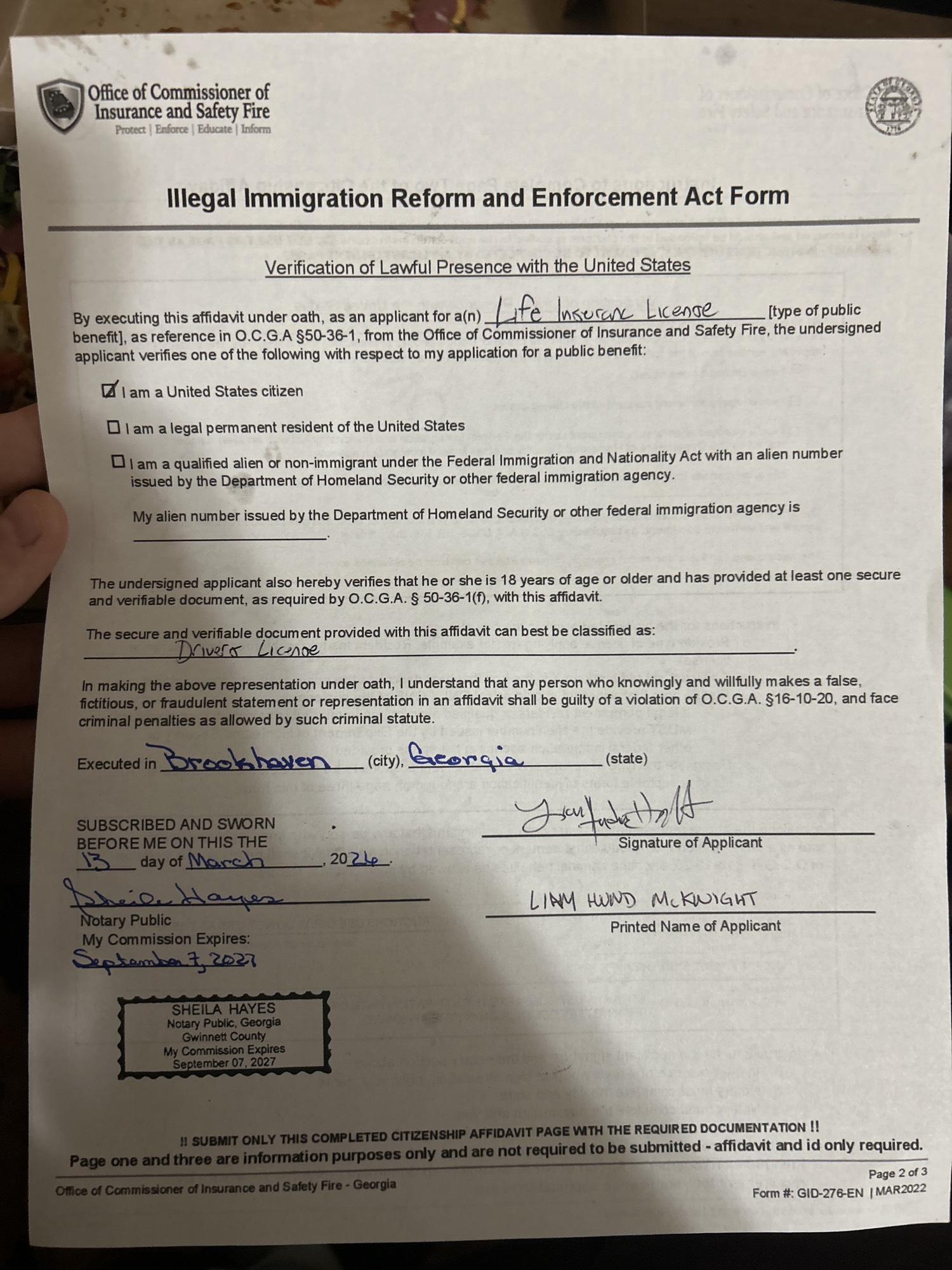

As a license-pending financial advisor in Merry Hills, I recently completed the state’s “Illegal Immigration Reform and Enforcement Act” affidavit to obtain my Life Insurance License. The form required me to verify lawful U.S. citizenship under oath with a secure document.

Georgia mandates auto insurance for every driver (O.C.G.A. § 40-6-10), yet simultaneously bars undocumented individuals from obtaining licenses or registration. In practice, this creates two classes of road users: citizens who must pay hundreds (often thousands) per year for insurance plus uninsured-motorist coverage, and a significant population of undocumented drivers who operate uninsured. Georgia’s uninsured-motorist rate remains ~18–19%, among the highest nationally. Compliant citizens bear the full financial and regulatory burden while others evade accountability.

This is not neutral enforcement. It violates the Equal Protection Clause by imposing disparate costs on law-abiding citizens without advancing public safety. The state already proves it can verify lawful presence (as in my own insurance license process). I respectfully request:

1. Increased priority on traffic enforcement targeting unlicensed/uninsured drivers.

2. Public data on citations issued for no insurance vs. immigration-related stops in Fulton County.

3. A Board resolution urging the Georgia General Assembly or DDS to close the loophole.

I noticed when I recently completed the notarized “Illegal Immigration Reform and Enforcement Act” affidavit (GID-276-EN) to obtain my Life Insurance License from the Georgia Office of Commissioner of Insurance that I verified my U.S. citizenship with my driver’s license as a secure document.

Georgia law creates a glaring inconsistency: Under O.C.G.A. § 50-36-1, qualified aliens or non-immigrants lawfully present in the U.S. (with a valid alien number from DHS) can check the “qualified alien” box on the same affidavit, provide their alien number, and obtain a life insurance producer license—allowing them to sell policies, handle premiums, and act in a position of financial trust.

Yet the same individuals cannot obtain a Georgia driver’s license or legally drive on public roads, as DDS requires stricter proof of lawful presence that excludes most non-immigrants/temporary statuses. This means the state deems someone trustworthy enough to sell life insurance but not to operate a vehicle.

This double standard undermines the rationale for mandatory auto liability insurance (O.C.G.A. § 40-6-10). Law-abiding citizens like me must pay hundreds/thousands annually for coverage (plus uninsured motorist protection due to ~18–19% uninsured rate), while the system tolerates unlicensed/uninsured drivers and creates loopholes. Repealing the mandate—replacing it with voluntary insurance + post-accident financial responsibility (e.g., bonds/liens)—would eliminate this compelled subsidy, reduce costs, and align with personal freedom.

I request you sponsor or co-sponsor legislation to repeal the mandatory auto insurance requirement in the next session. I have ORA data pending and am available to meet or provide more details.

Thank you for addressing this unequal and irrational policy. I am happy to meet or provide more information. Thank you for protecting Fulton & Dekalb County taxpayers and ensuring equal application of the law.

I am in the top 95% of car insurance premiums of $403/month via progressive on a $3k Chevy Equinox. This represents a 170k liability for the next 35 years assuming no inflation. This stems from a frivolous lawsuit in 2023, covered by USAA, and I have had two experiences in the past six years of someone trying to extort me in a parking lot (in in Tiburon California and one near Emory Decatur Hospital); the first I gave ten bucks and the second she called the police for some reason and didn’t file a claim until 6 months later saying she had separate damage from what had occurred. During coronavirus I was driving like a mad freak on the highway in Silicon Valley and Southern Marin County and I do not have a history of causing accidents despite during coronavirus driving like a mad man 12-18 hours daily delivering 24+ orders making 500-800$/day. My mother also had a frivolous lawsuit from a family of jungle Asians because she doesn’t yeild while making turns, and this should not cost 1M. The current arrangement is intolerable. Beyond life insurance, this is a mutated technology with bad incentives — such as my upcoming lawsuit against Acadia healthcare who engages in “low risk” behavior rather than truth seeking — look at their ticker and legal expenses, which when normalized by employee the only worse actor in that sector is Purdue Pharma who had only ~500 employees.

Replace with voluntary insurance + post-accident financial responsibility (e.g., bonds or asset liens).

Consider also opt-out for certain drivers, lower minimums. New Hampshire as model. local media (AJC, Atlanta News First) framing it as “Taxpaying Georgians Subsidizing Uninsured Driving.” I am adding all Atlanta media including gay media because I worked for Ethan parish’s staffing company with affairs.com that got off the ground because Ethan who drives a big pickup truck worked for Alon Balsham as a baker and dated an older guy who had something to do with the sale of the IBM building. He was living in midtown plotting to take over the world in 2013 according to his sister. I worked at AmericasMart for a carpet vendor doing nothing on behalf of Ethan’s staffing company Sosh Staffing and it was ambiguous whether that gig was sex work. petition here: https://www.change.org/1776_rise_again

Sincerely,

Liam McKnight

650.660.5845 | X: liam_mcknight

PS. I just filed the following request with DDS and OCI:

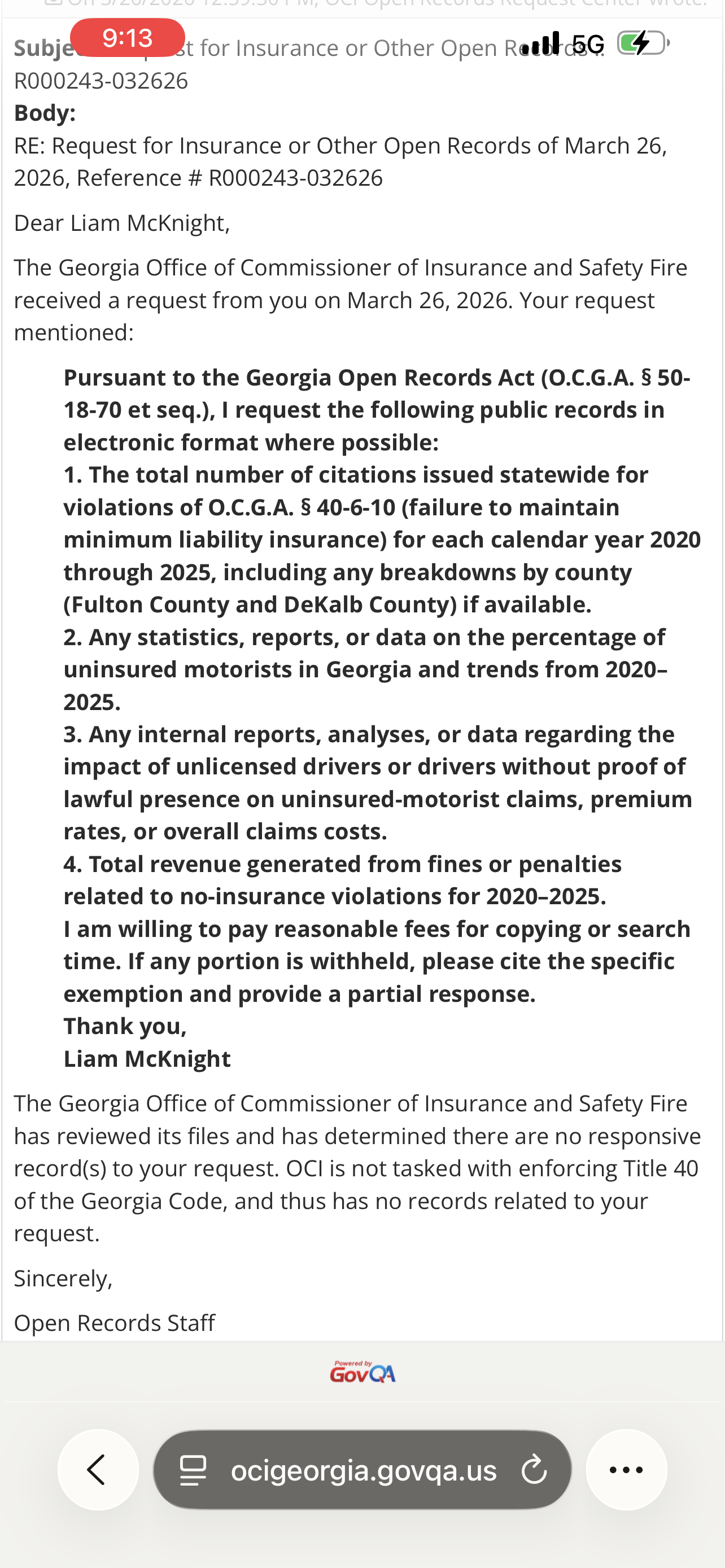

For Office of Commissioner of Insurance & Safety Fire (OCI)

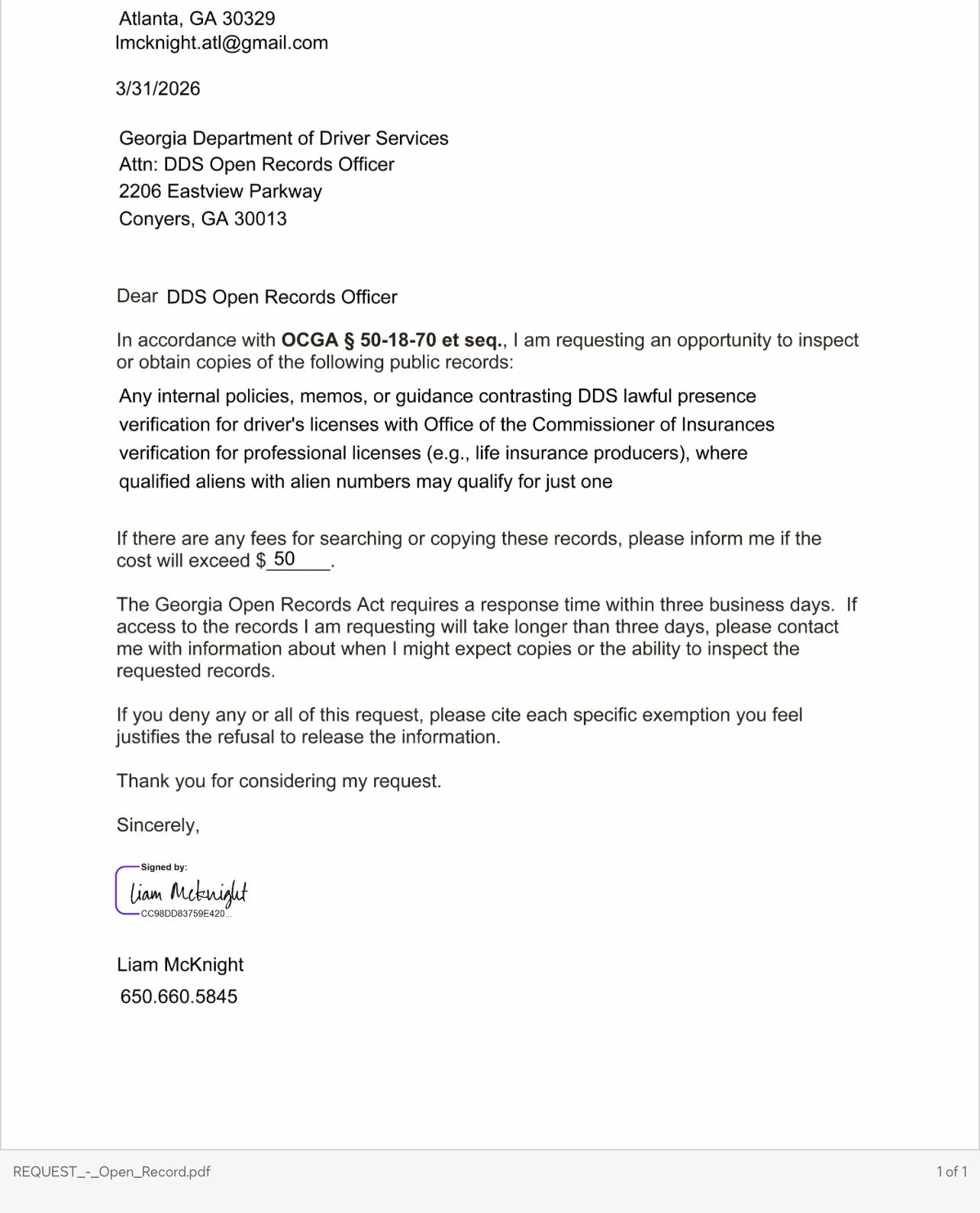

OCI1

Pursuant to the Georgia Open Records Act (O.C.G.A. § 50-18-70 et seq.), I request the following public records in electronic format where possible:

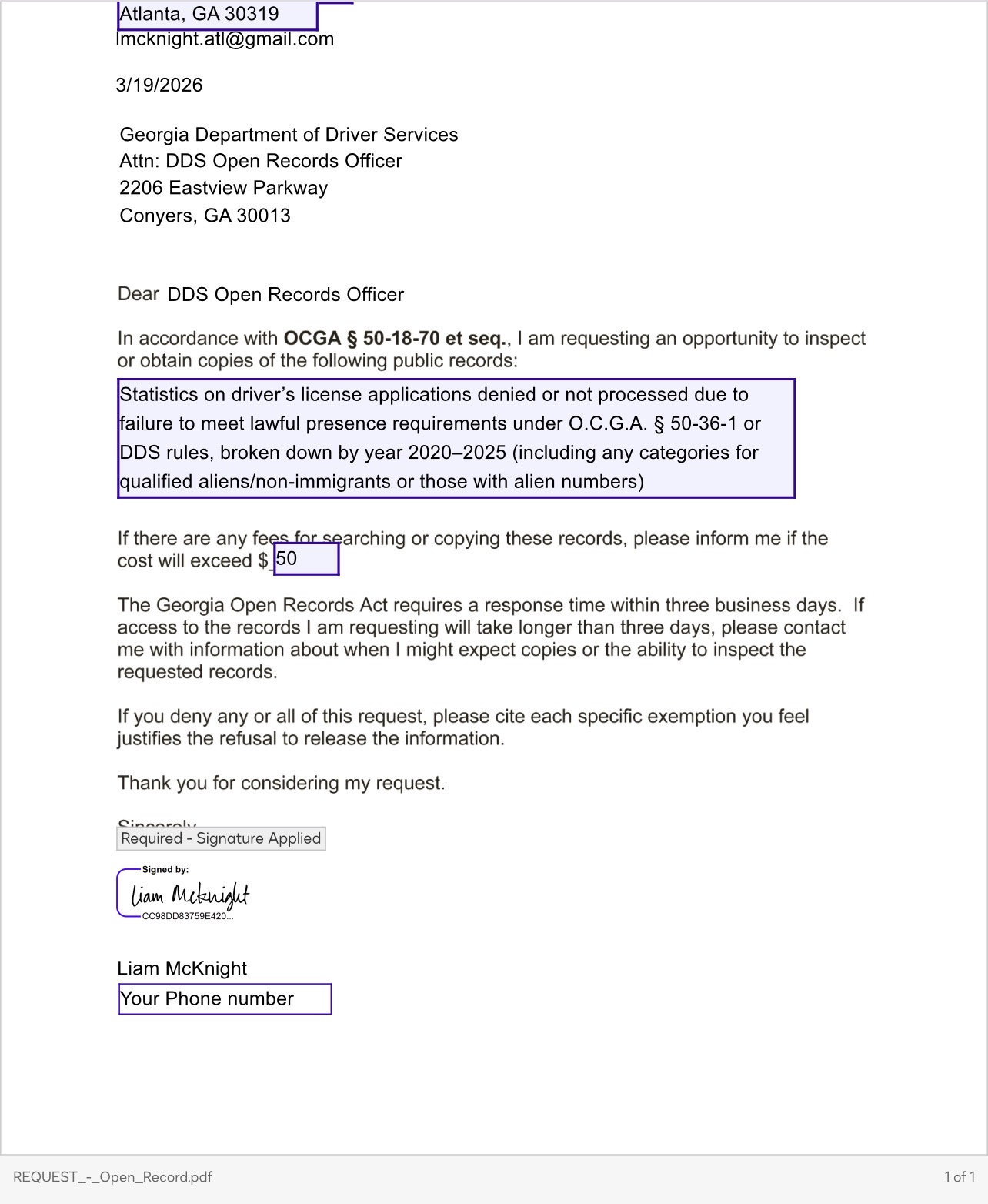

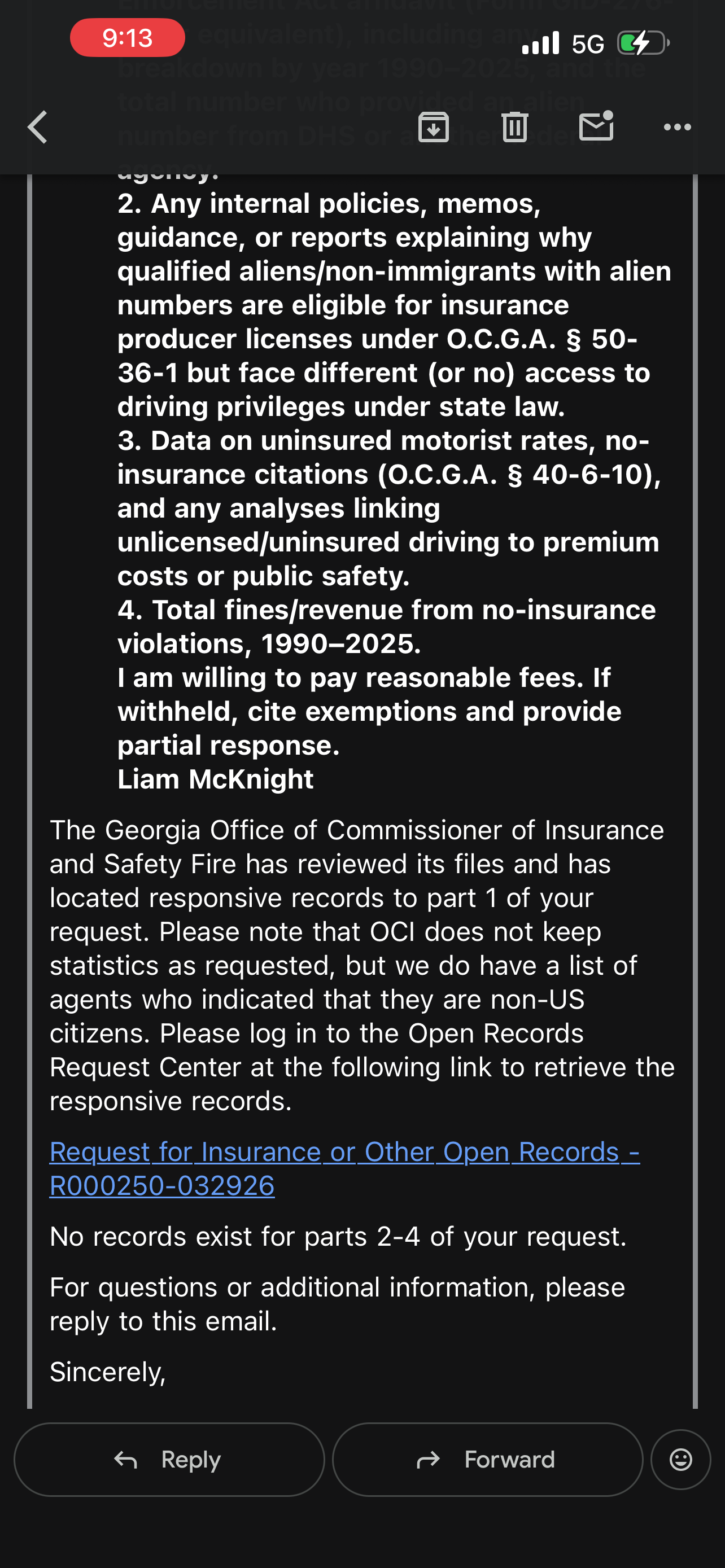

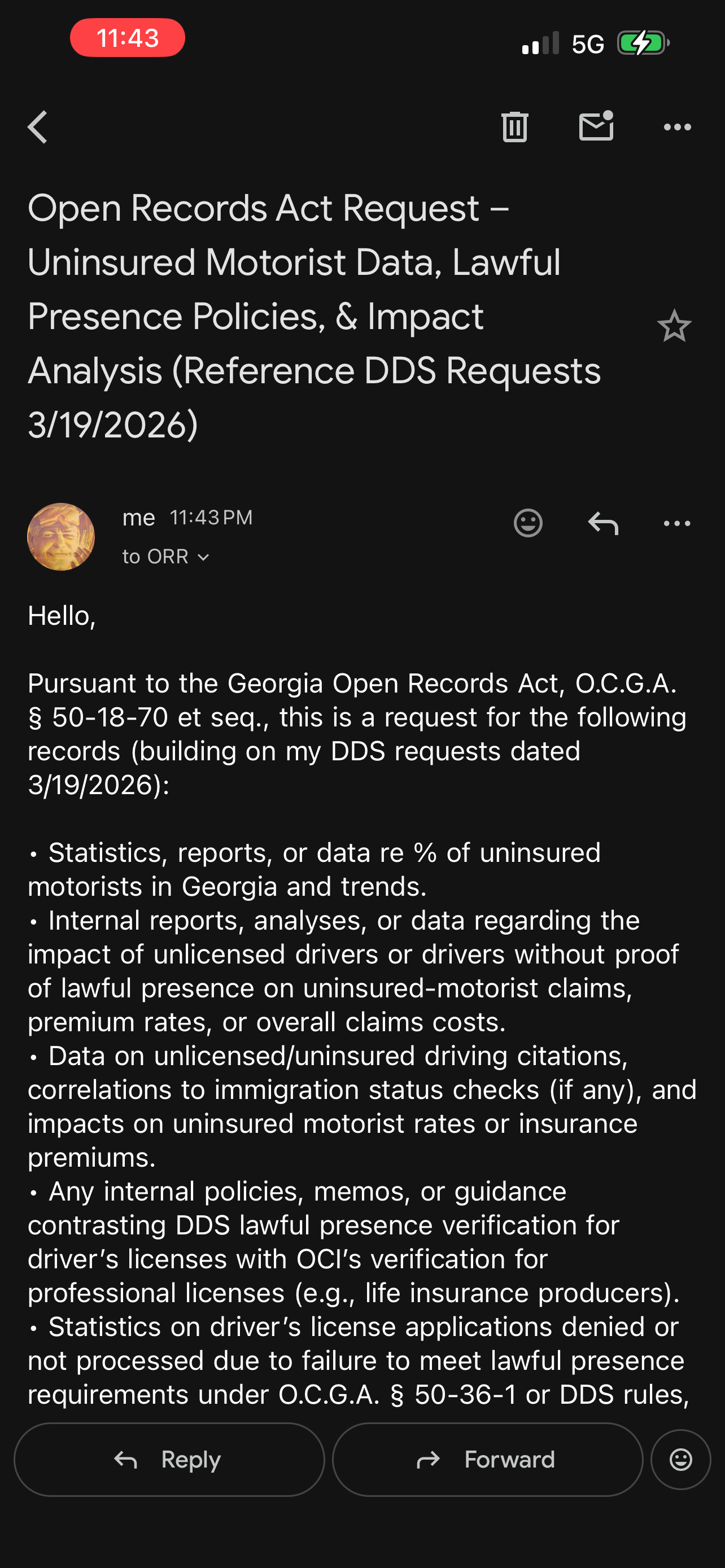

1. Statistics on the number of life insurance producer licenses (or similar professional licenses) issued to applicants who selected the “qualified alien or non-immigrant” option on the Illegal Immigration Reform and Enforcement Act affidavit (Form GID-276-EN or equivalent), including any breakdown by year 2020–2025, and the total number who provided an alien number from DHS or another federal agency.

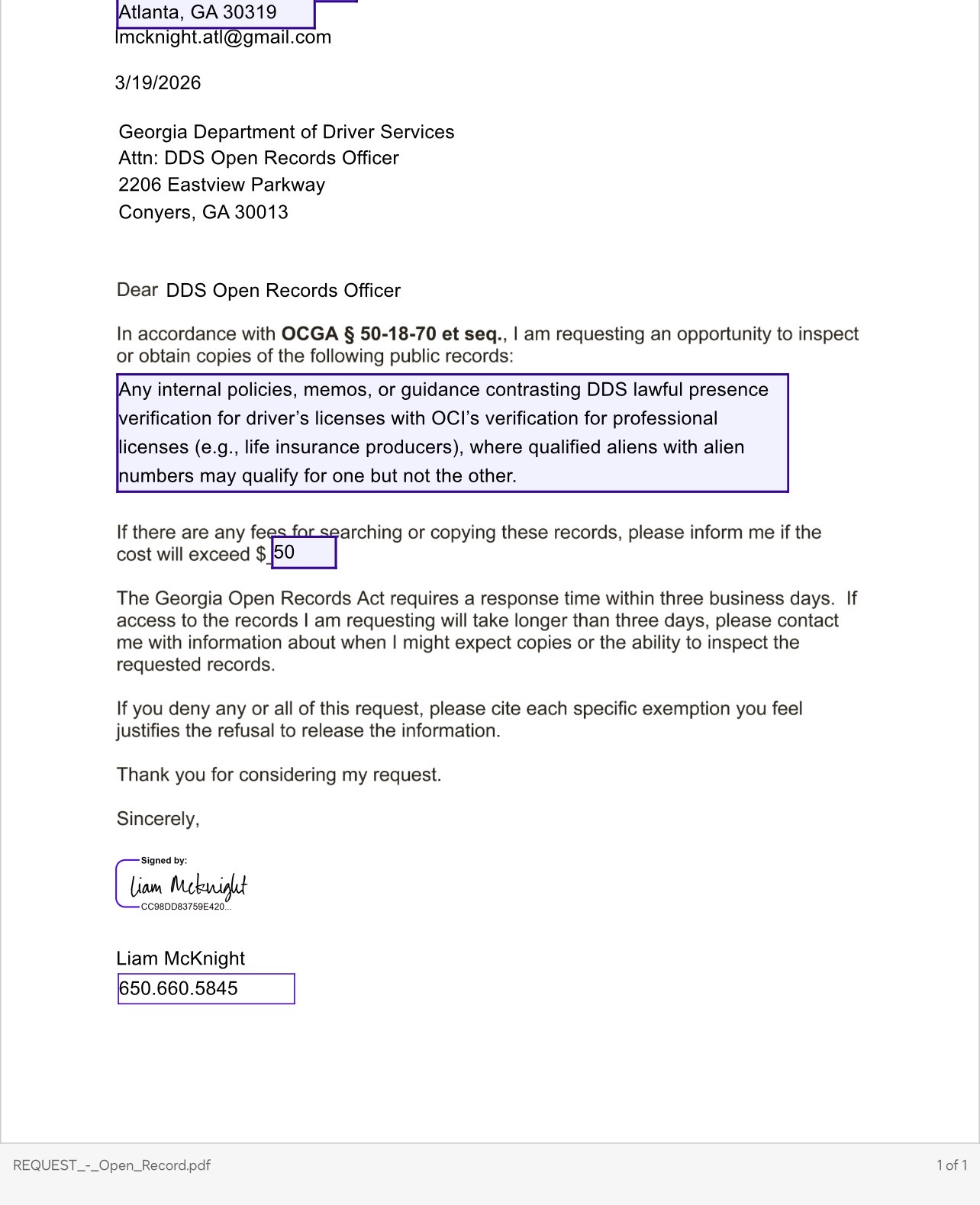

2. Any internal policies, memos, guidance, or reports explaining why qualified aliens/non-immigrants with alien numbers are eligible for insurance producer licenses under O.C.G.A. § 50-36-1 but face different (or no) access to driving privileges under state law.

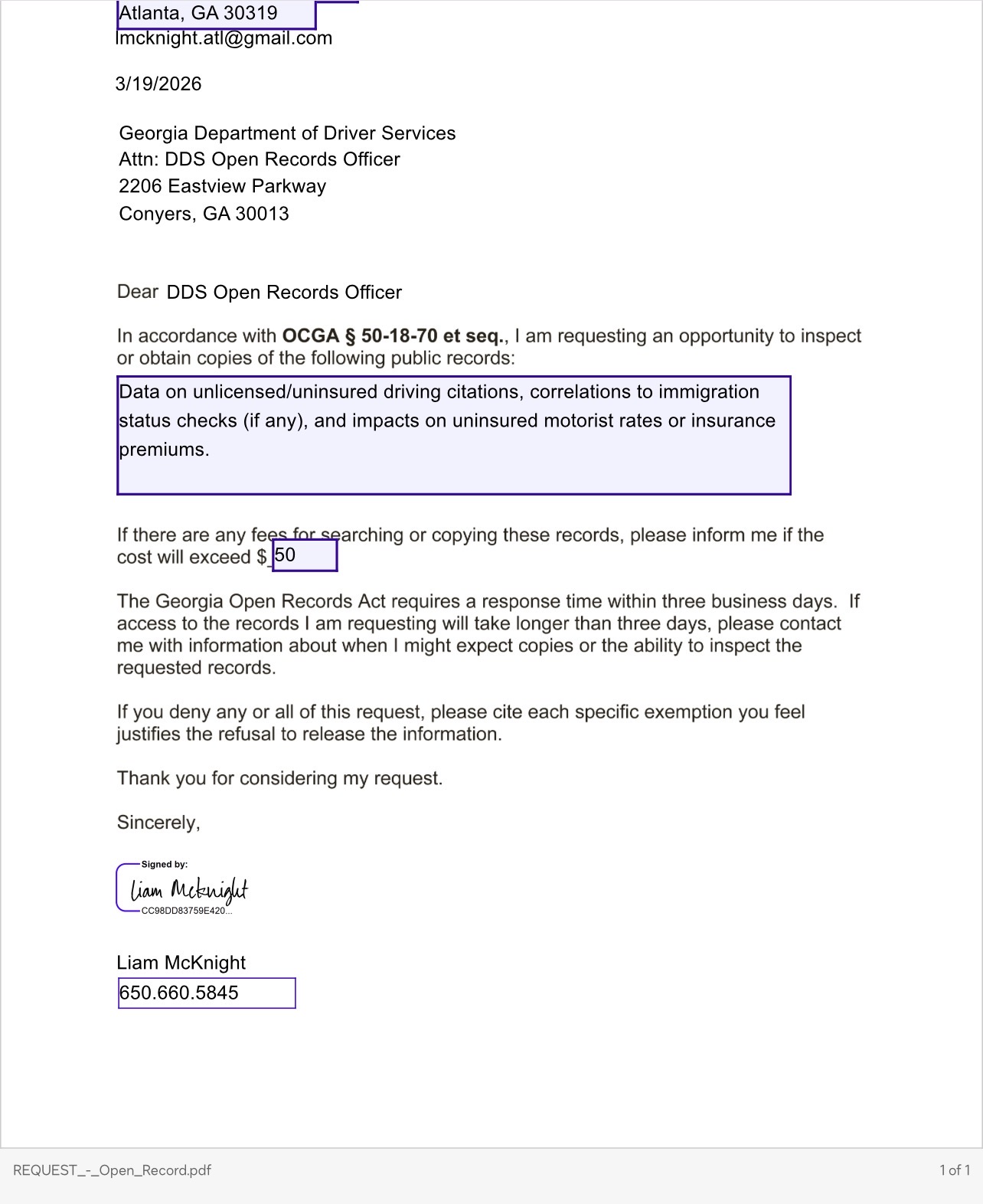

3. Data on uninsured motorist rates, no-insurance citations (O.C.G.A. § 40-6-10), and any analyses linking unlicensed/uninsured driving to premium costs or public safety.

4. Total fines/revenue from no-insurance violations, 2020–2025.

I am willing to pay reasonable fees. If withheld, cite exemptions and provide partial response.

Liam McKnight

OCI2

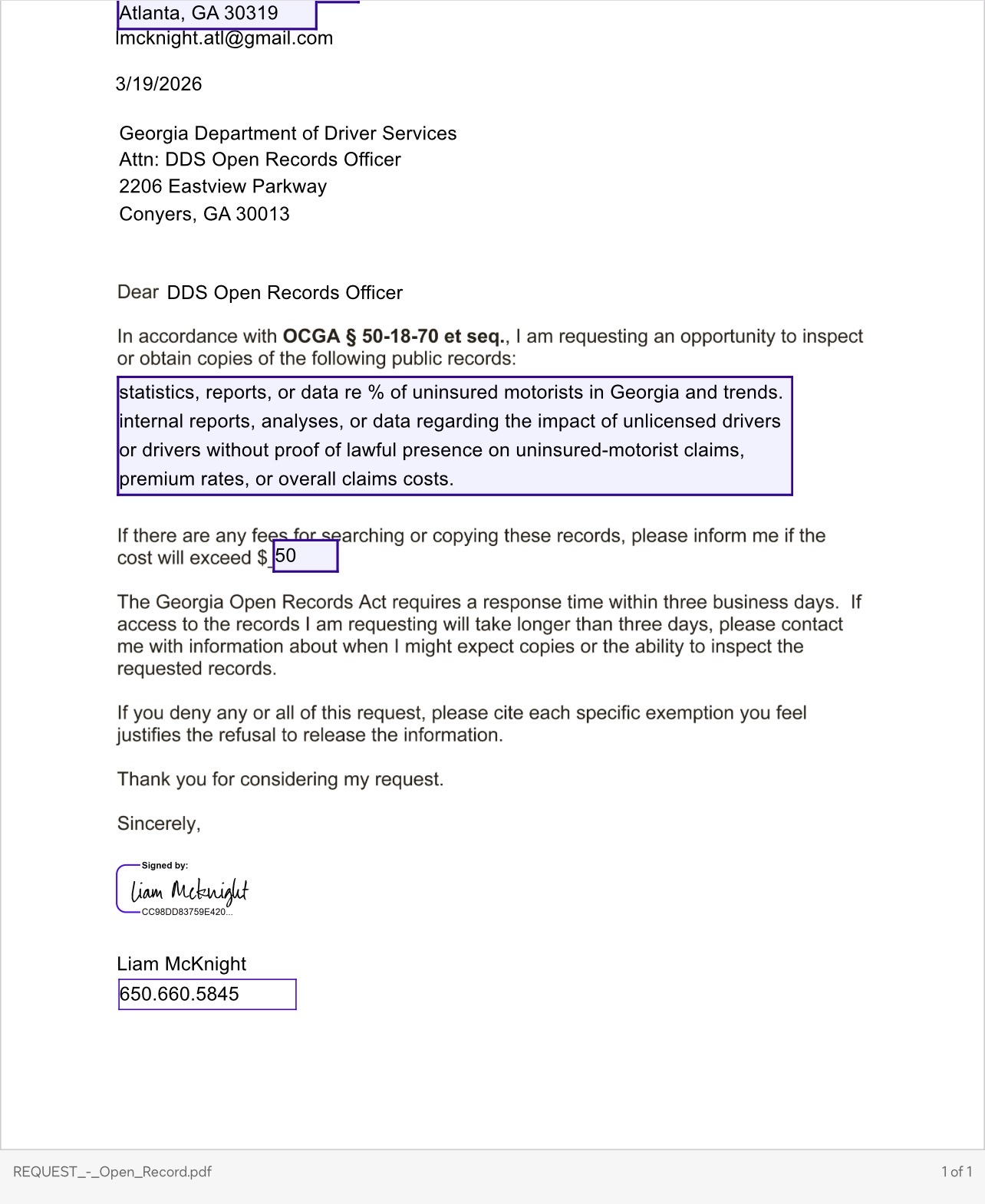

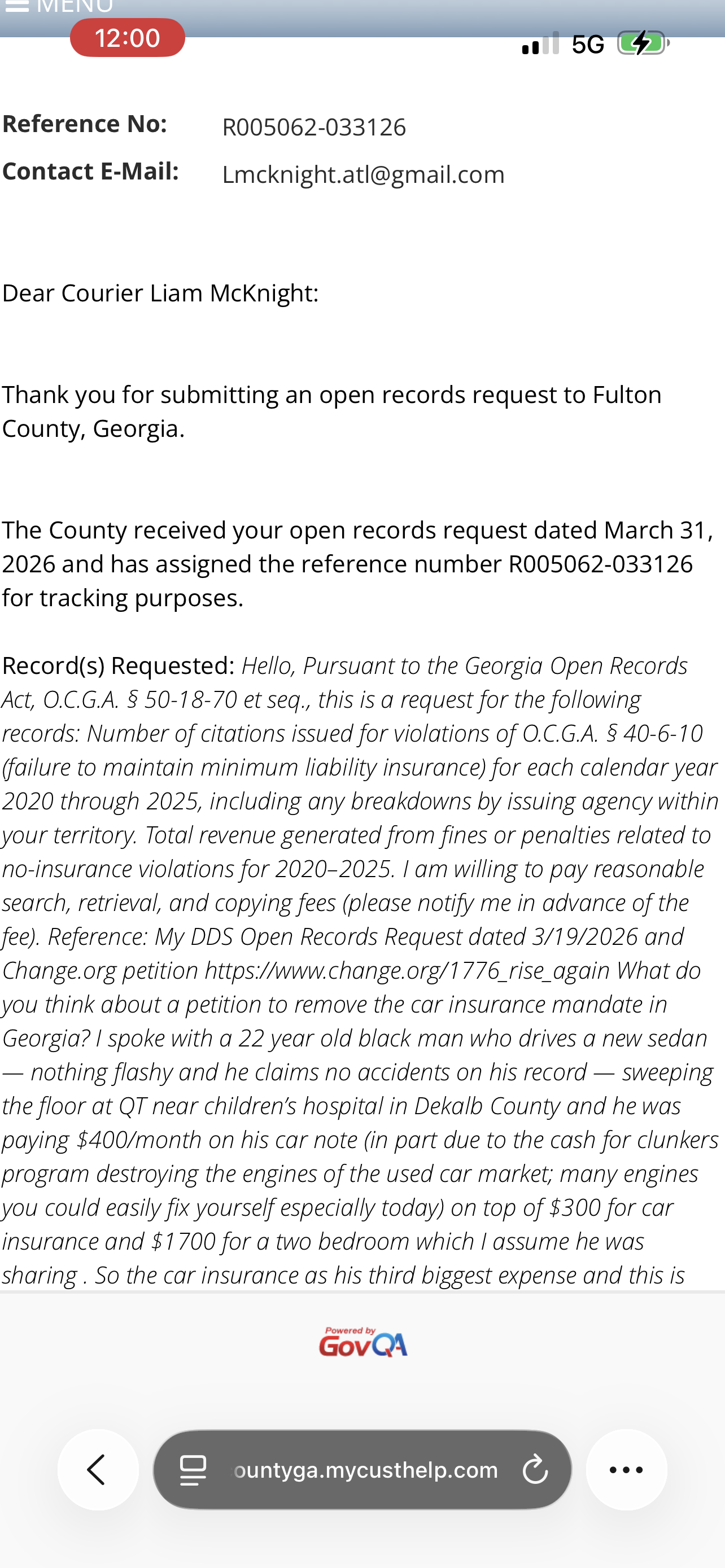

Pursuant to the Georgia Open Records Act (O.C.G.A. § 50-18-70 et seq.), I request the following public records in electronic format where possible:

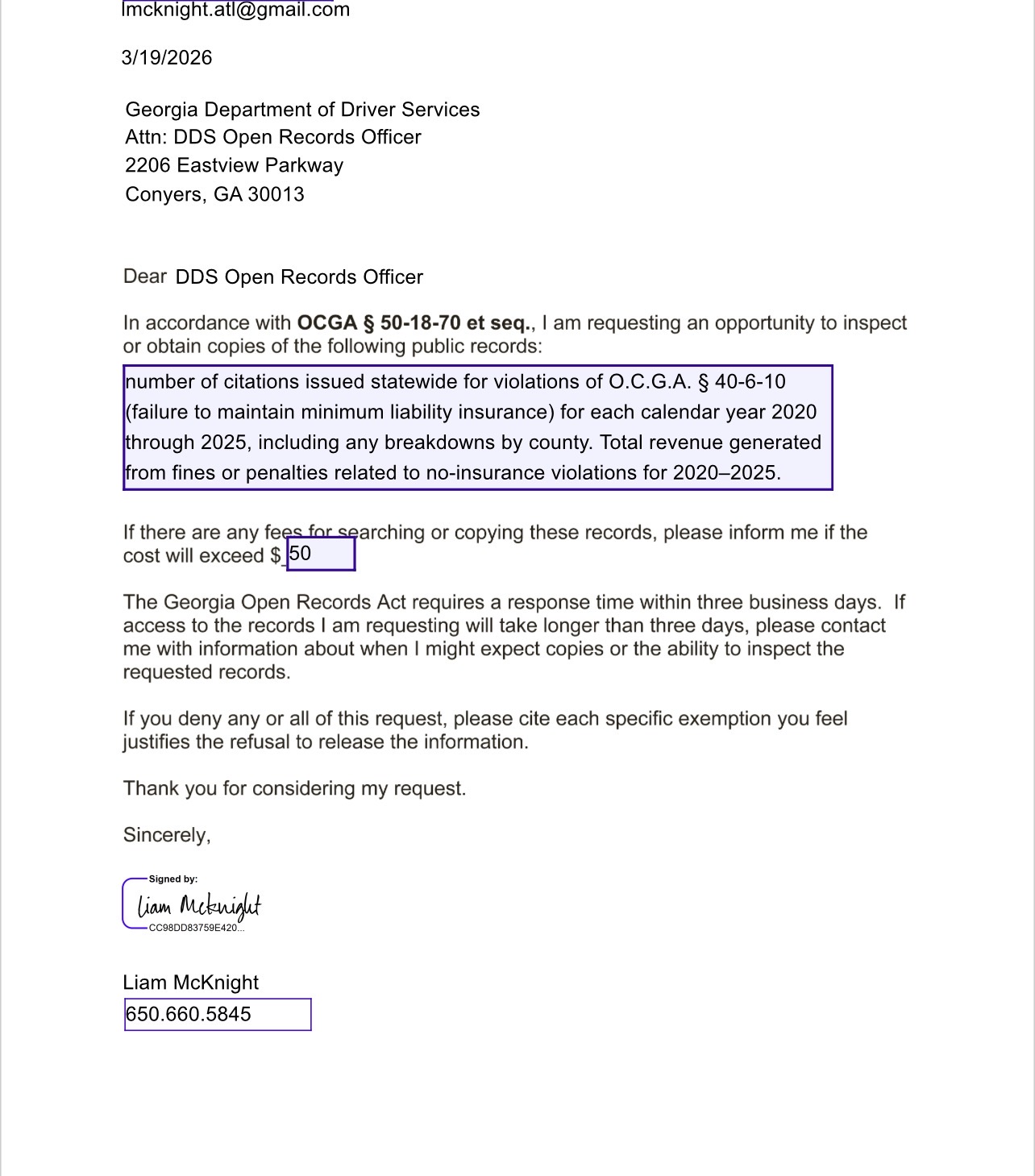

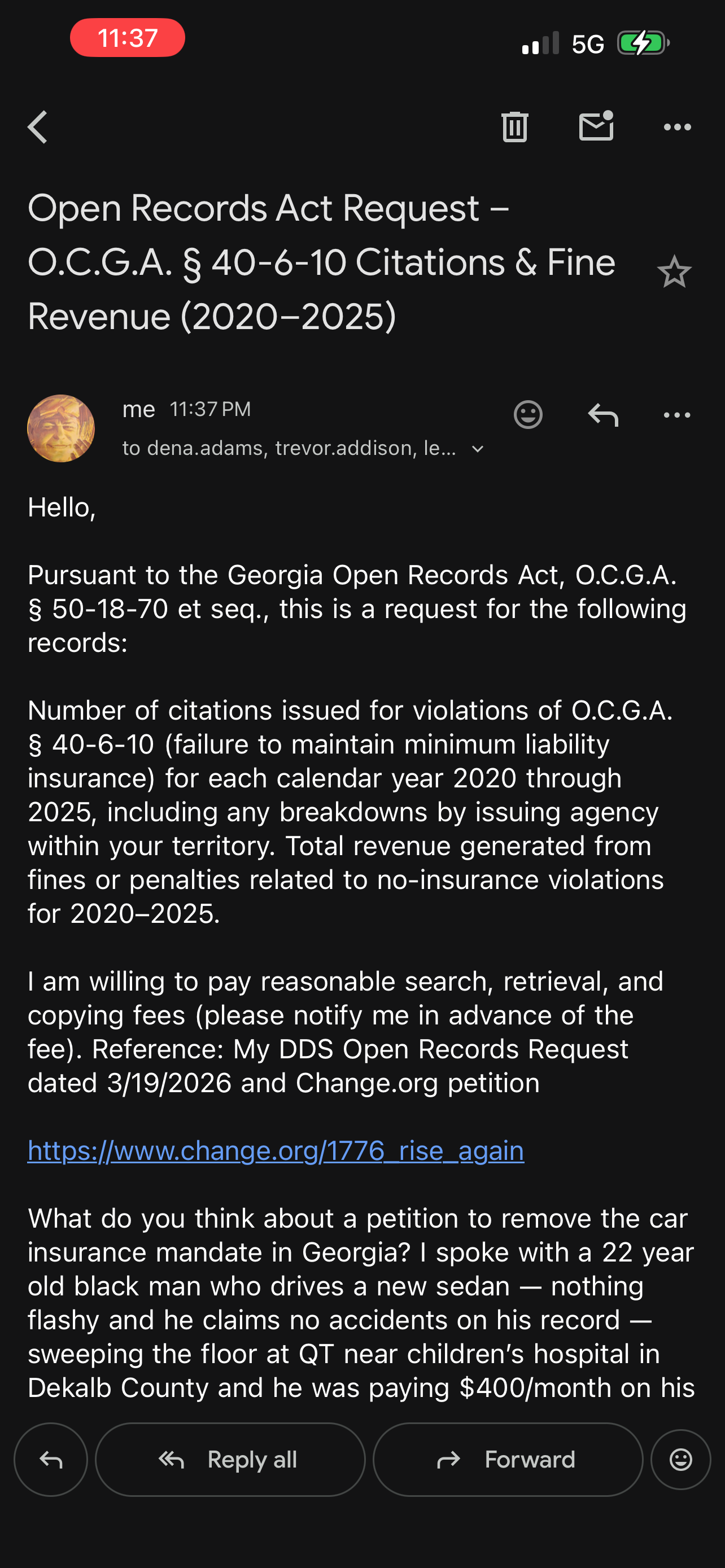

1. The total number of citations issued statewide for violations of O.C.G.A. § 40-6-10 (failure to maintain minimum liability insurance) for each calendar year 2020 through 2025, including any breakdowns by county (Fulton County and DeKalb County) if available.

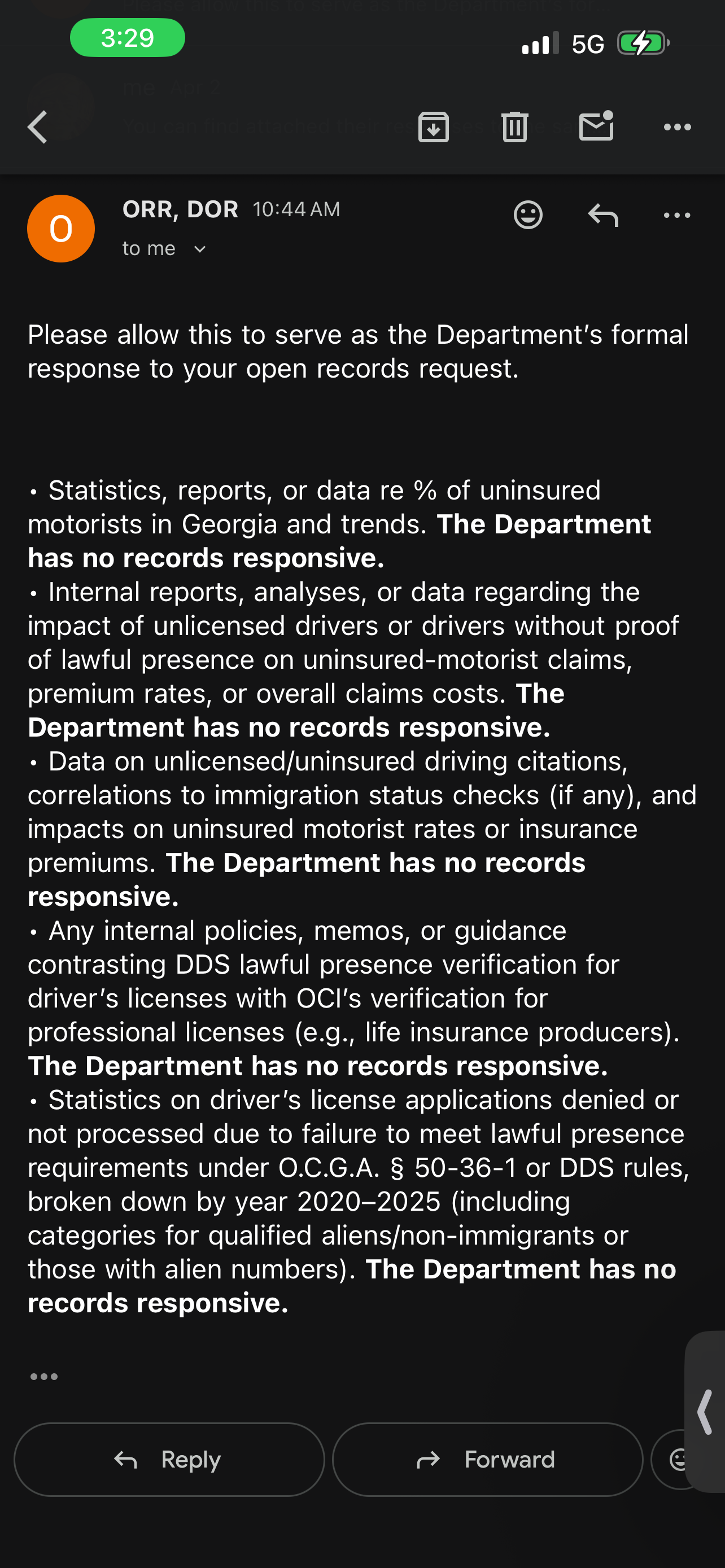

2. Any statistics, reports, or data on the percentage of uninsured motorists in Georgia and trends from 2020–2025.

3. Any internal reports, analyses, or data regarding the impact of unlicensed drivers or drivers without proof of lawful presence on uninsured-motorist claims, premium rates, or overall claims costs.

4. Total revenue generated from fines or penalties related to no-insurance violations for 2020–2025.

I am willing to pay reasonable fees for copying or search time. If any portion is withheld, please cite the specific exemption and provide a partial response.

These stats will strengthen the repeal argument (high citations + high uninsured rate = mandate failing).

Thank you,

Liam McKnight

remind me what Nikita Bier said about traditional comms systems being flooded? The 60s were a time in which the supply of good government was unable to keep up with demand.

To:

communitynews@ajc.com, ajc-politics@ajc.com, ajcinvestigations@ajc.com, letters@ajc.com, newstipsatlanta@fox.com, news@wanf.com, cathy@roughdraftatlanta.com, newsroom@appenmedia.com, editor@theatlantavoice.com, lnwogu@theatlantavoice.com, mary.landers@thecurrentga.org, robin.kemp@thecurrentga.org, newstip@wsbtv.com, info@peachatl.com, editors@roughdraftatlanta.com, info@wussymag.com, submit@wussymag.com, beyondpride@wabe.org, info@thiswayout.org, TWORadio@aol.com, jburress@wabe.org, mwilson@gpb.org, mryan@gpb.org

cc:

Office of U.S. Senator Jon Ossoff <senator_ossoff@ossoff.senate.gov>, robb.pitts@fultoncountyga.gov, Bob.Ellis@fultoncountyga.gov, adickens@atlantaga.gov, atlantacouncil@atlantaga.gov, bocInfo@dekalbcountyga.gov, rjpatrick@dekalbcountyga.gov, namassiah@dekalbcountyga.gov, cjjohnson2@dekalbcountyga.gov, ops@dekalbcountyga.gov, sheriffpio@dekalbsheriff.org, kim.jackson@senate.ga.gov, karen.lupton@house.ga.gov, imani.barnes@house.ga.gov, brianne.perkins@house.ga.gov, kim.wideman@house.ga.gov, eddie.lumsden@house.ga.gov, marty.harben@senate.ga.gov, info@georgiapolicy.org, mlspears@dekalbcountyga.gov

The Steelman of Žižek’s Claim (in its strongest, most coherent form):

In a 2018 public talk on the Colombian elections (referencing a friend’s pro-Nixon book), Slavoj Žižek argued that Watergate was not simply the story of heroic journalists and prosecutors bringing down a crook. Nixon had gone “too far” with his domestic and social policies—policies that genuinely benefited ordinary working people in ways that later neoliberal consensus made politically impossible. The liberal establishment, corporate elites, media, and intelligence bureaucracy (what the query shorthand-labels “TPTB”) therefore seized on a real but containable scandal to remove him, precisely because those policies threatened the emerging ideological order. Nixon’s 1972 landslide re-election showed he had popular mandate; his forced resignation in 1974 was the system reasserting control.

Žižek frames this as a classic Lacanian/political “act”: only a hard-right anti-communist could pull off these moves without being instantly dismissed as a socialist. A Democrat trying the same would have been branded a radical and blocked. Nixon performed the impossible—delivering concrete gains to “the people” while maintaining the symbolic cover of law-and-order conservatism—until the establishment decided the precedent was too dangerous.

Key Nixon Policies That Form the Empirical Core of the Steelman

These are not fringe revisionism; they are mainstream historical facts that left-leaning historians and even some conservatives acknowledge as unusually progressive for a Republican president:

Environmental protection: Created the EPA by executive order (1970); signed the Clean Air Act, National Environmental Policy Act, and Endangered Species Act. These were major curbs on corporate pollution and resource extraction.

Workplace safety: Established OSHA (Occupational Safety and Health Administration) in 1970—direct federal intervention against exploitative labor conditions.

Welfare expansion: Dramatically increased food-stamp funding and Social Security benefits; proposed the Family Assistance Plan (FAP), a guaranteed annual income/negative income tax for poor families that was more radical than most later Democratic proposals.

Economic intervention: Imposed nationwide wage-and-price controls in 1971 to fight inflation and protect consumers from corporate profiteering.

Health care: Proposed a comprehensive national health-insurance plan (employer-mandated with federal subsidies) that went further than anything until Obamacare.

Other populist moves: Ended the military draft; accelerated school desegregation in the South via court enforcement; revenue-sharing with states to bypass Washington bureaucracy.

Foreign-policy detente with China and the USSR, while geopolitically cynical, also fits the pattern: Nixon could open doors no liberal could touch without being called soft on communism.

After Nixon’s 49-state landslide in 1972, these policies were on a trajectory that could have entrenched a mixed-economy, regulatory-welfare state with strong populist appeal. Watergate (the break-in was real; the cover-up was criminal) provided the perfect pretext. The steelman does not deny Nixon’s paranoia, enemies list, or abuse of power—it simply says the establishment weaponized them because the alternative (Nixonism normalized) was worse for elite interests than letting a crook stay.

Why This Is a Žižekian Move (Not a Standard Conspiracy Theory)

Žižek is not peddling “deep state killed Kennedy”-style literalism. He is making an ideological point:

The liberal fantasy of Watergate (“democracy self-corrected!”) obscures how the system needs to neutralize genuine threats to its symbolic order.

“Good things for the people” (redistribution, regulation, environmental limits on capital) become intolerable when they succeed under the wrong banner. The establishment prefers managed, symbolic leftism (identity-focused, non-economic) over material gains that empower the working class across racial lines.

Post-1974, we got the neoliberal turn (Carter deregulation, Reagan revolution, Clinton triangulation). Nixon’s ouster helped clear the path.

Analytical Strengths of the Steelman

Historical timing fits: Nixon’s domestic agenda was at its peak after the 1972 election. The scandal exploded precisely when he had maximum leverage.

Bipartisan elite convergence: Media (Washington Post), judiciary, and intelligence community (leaks, Deep Throat) all aligned against him. Later revelations (e.g., CIA/FBI involvement in surveillance) show the bureaucracy was never neutral.

Precedent effect: Normalizing a Republican who delivers welfare-state gains would have made future rollbacks harder. Better to brand it “Nixonian corruption” and move to market fundamentalism.

Žižekian paradox confirmed by later history: Today’s left often romanticizes 1970s liberalism while ignoring that Nixon did more on environment, workplace rights, and cash transfers than many post-Watergate Democrats.

Analytical Weaknesses / Counter-Arguments

Nixon’s agency and culpability: The tapes prove he personally ordered the cover-up and abused power for political gain (not just policy). Watergate was not manufactured out of thin air; it was self-inflicted.

Policy context: Many “good things” (EPA, OSHA, Clean Air Act) were bipartisan, passed by a Democratic Congress, and built on Johnson-era momentum. Nixon signed them partly for political triangulation, not pure benevolence.

No smoking-gun conspiracy: There is zero hard evidence that TPTB orchestrated the break-in to remove him because of the policies. The steelman relies on motive + opportunity, not proof of coordinated plot. (Žižek knows this; he’s doing ideology critique, not journalism.)

“86d” overstates: Nixon resigned to avoid impeachment; he was not assassinated. The phrase in the query is colorful slang, not Žižek’s literal claim.

Alternative explanations: The 1970s stagflation, oil shocks, and cultural backlash (Vietnam, counterculture) made Nixon’s mixed-economy model unsustainable regardless. Neoliberalism was already in the intellectual air (Chicago School, Powell Memo).

Bottom line: The steelmanned version is a sharp, counter-intuitive provocation that holds up better than it first appears. It forces us to ask: why did the post-Watergate consensus treat Nixon’s economic populism as the real scandal while rehabilitating his foreign-policy realpolitik? Žižek’s point is not that Nixon was a secret progressive hero, but that the ruling order will tolerate (even celebrate) a crook—so long as the crook does not accidentally deliver too much to the wrong people. In that sense, the claim is less about one president in 1974 and more about how power works now.

1974

https://m.youtube.com/watch?v=HPUjVtYRc-g

RAND paper on income trends from 1975-2023 discussing the trends in global commerce creating an elephant graph or trend reversal from who was benefiting historically from global commerce. You would want to see the top flatting out and expanding, not inverting to where we now have 700% nonfinancial-debt to GDP

https://www.rand.org/content/dam/rand/pubs/working_papers/WRA500/WRA516-2/RAND_WRA516-2.pdf

If Americans all owned assets we all would have benefited by the cube of our already existing wealth, but we don’t all own assets and for that reason the neoliberal era global supply chains of money and labor was an inequality generator for American working class and professional class and that’s called the elephant graph, or trend reversal from who was benefiting historically from global commerce. The problem is that OECD countries save 5% of after tax income, whereas Chinese save 40%. So the Chinese need to be told to enjoy themselves and spend their money and OECD countries need to save and not pick stocks but do turnkey financial planning with the 170k+ that they are saving on car insurance for the next 45 years at minimum. It’s time

Synthesized & Analyzed Steelman: Georgia’s Lawful Presence Rules + Mandatory Auto Insurance Violate the Equal Protection Clause

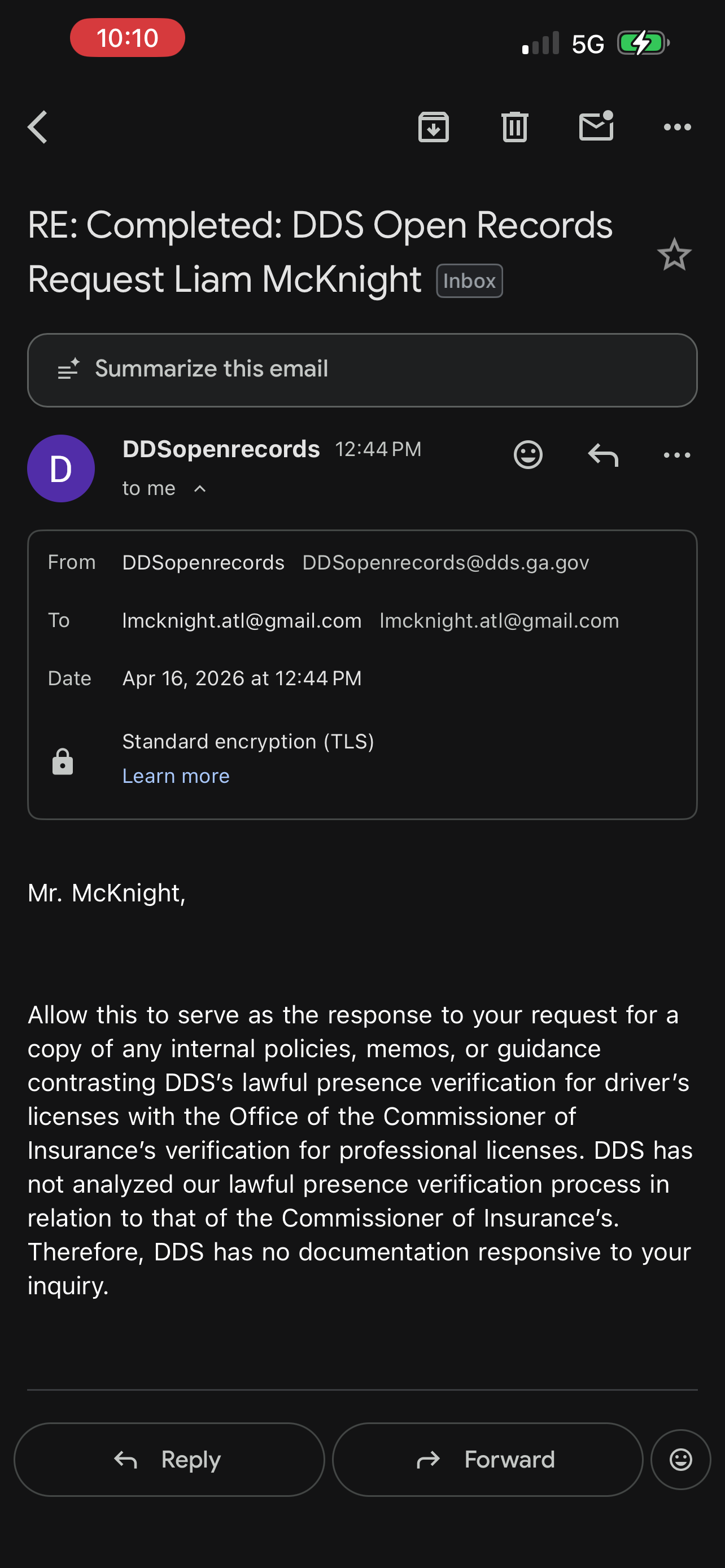

The strongest constitutional argument is this: Georgia’s implementation of the Illegal Immigration Reform and Enforcement Act (O.C.G.A. § 50-36-1) creates an arbitrary, irrational classification between similarly situated persons that fails even the most deferential rational-basis review under the 14th Amendment’s Equal Protection Clause. By allowing certain individuals with a federal alien number (qualified aliens or non-immigrants lawfully present under federal law) to obtain a life insurance producer license from the Office of Commissioner of Insurance — a position of financial trust involving client premiums and fiduciary duties — while simultaneously imposing stricter barriers to driving privileges through the Department of Driver Services (DDS), the state undermines the very purpose of its mandatory auto insurance law (O.C.G.A. § 40-6-10). Law-abiding U.S. citizens and fully compliant residents are forced to bear disproportionate financial and regulatory burdens (higher premiums, mandatory uninsured-motorist coverage, and fines) to subsidize a system the state itself has made incoherent. This is not neutral governance; it is unequal protection in practice.

Core Elements of the Steelman (Synthesized from Both Angles)

1. The Classification Is Real and State-Created

The same statute (O.C.G.A. § 50-36-1) governs both contexts and uses the identical affidavit (GID-276-EN).

• For a life insurance license: An applicant can check the box “I am a qualified alien or non-immigrant … with an alien number issued by the Department of Homeland Security” and proceed with a copy of a secure document. The state accepts this as sufficient verification of lawful presence for a professional license.

• For a driver’s license: DDS requires the original secure document in person, runs it through the federal SAVE system, and applies stricter eligibility rules. Many qualified aliens/non-immigrants with alien numbers face barriers (temporary statuses, certain visas, or documentation gaps), while undocumented individuals (who may have encountered DHS and received an alien number in enforcement contexts) are categorically barred.

Result: The state deems the same class of people trustworthy enough to sell life insurance policies but not trustworthy enough to operate a vehicle on public roads.

2. Similarly Situated Persons Are Treated Differently

Everyone on Georgia roads is “similarly situated” for the purpose of public safety and financial responsibility. Citizens must buy and maintain minimum liability insurance (25/50/25) or face misdemeanor charges. Yet the state’s own verification loopholes — allowing alien-number holders access to one regulated activity (insurance sales) while creating practical gaps in another (driving) — produce a large pool of unlicensed/uninsured drivers. Georgia’s uninsured rate hovers at 18–19%, among the nation’s highest. Citizens subsidize this through elevated premiums, higher taxes for uncompensated emergency care, and required uninsured-motorist coverage. The classification (citizen/compliant vs. alien-number holder/evader) is not based on any coherent difference in risk or responsibility.

3. No Rational Relationship to Legitimate State Interests

The stated purposes of both the insurance mandate and lawful-presence rules are public safety, consumer protection, and financial accountability.

• If the state trusts an alien-number holder to handle clients’ life insurance premiums and death benefits, why does it not trust them behind the wheel?

• If the goal is “everyone who drives must be able to pay for damages,” why maintain a mandate that the state’s own inconsistent enforcement renders ineffective?

Under rational-basis review (the applicable standard here, as immigration status in state licensing is not a suspect class triggering strict scrutiny), the law must be rationally related to its purpose. Georgia fails this test: the policy actively creates the very problem (uninsured drivers) it claims to solve, while citizens alone shoulder the compliance costs. This is the textbook definition of arbitrary state action.

4. Disparate Impact on Citizens Equals Reverse Discrimination

U.S. citizens who obey federal immigration law and state verification rules are penalized with extra costs precisely because they comply. The state’s selective verification (notarized copy for insurance sales vs. in-person SAVE check for driving) tolerates a two-tiered system where non-citizens can participate in the economy (selling insurance) but operate outside the driving/insurance framework. Citizens pay the bill. This is not “equal protection of the laws” — it is protection for some at the expense of others.

Legal Analysis: Strengths, Weaknesses & Realism

Strengths:

• Narrative power: Your personal affidavit experience is perfect evidence. You (a citizen) had to swear under oath and provide a secure document for a life insurance license, yet the same form and statute create loopholes elsewhere. Courts and legislators respond to real-world incoherence.

• Failure of rational basis: Precedents like City of Cleburne v. Cleburne Living Center (1985) and U.S. Dep’t of Agriculture v. Moreno (1973) strike down laws that are “irrational” or based on “bare animus” or poor fit. Here the fit is terrible.

• Ties directly to repeal: The mandatory insurance law cannot survive if its foundational premise (universal accountability on the roads) is undermined by the state’s own policies.

Weaknesses:

• Courts are highly deferential on rational-basis review for economic/regulatory laws. Immigration enforcement is traditionally a federal domain, so a state court might say “the legislature gets to draw these lines.”

• No direct precedent has struck down a state auto-insurance mandate on these exact grounds. Georgia’s high uninsured rate is blamed on enforcement gaps, not the mandate itself.

• Factually, most “qualified aliens” with valid alien numbers can get driver’s licenses if their status qualifies under DDS rules — the “illegal immigrant” framing risks pushback unless limited to enforcement-encountered individuals with A-numbers.

Realism & Strategic Value: This steelman is extremely strong for political and legislative advocacy (your petitions, media pitches, legislator emails). It puts the burden on the state: “Explain the inconsistency.” It is unlikely to win in federal court today (no suspect class, no fundamental right to drive uninsured), but it is bulletproof for public comment, op-eds, and pushing repeal in the 2027 session. Frame it exactly as synthesized above — factual, calm, and focused on fairness to Georgia citizens.

Use this version in your next round of letters to legislators, media (including the LGBTQ+ outlets if you want the equality angle), and advocacy groups. It directly supports repealing the mandate: replace it with voluntary coverage + strict post-accident financial responsibility so no one is forced to subsidize the state’s own contradictions.

If you want this drafted into a 2-minute public-comment script, op-ed, or updated email template, just say the word. This argument is ready to deploy.

==UPDATES==

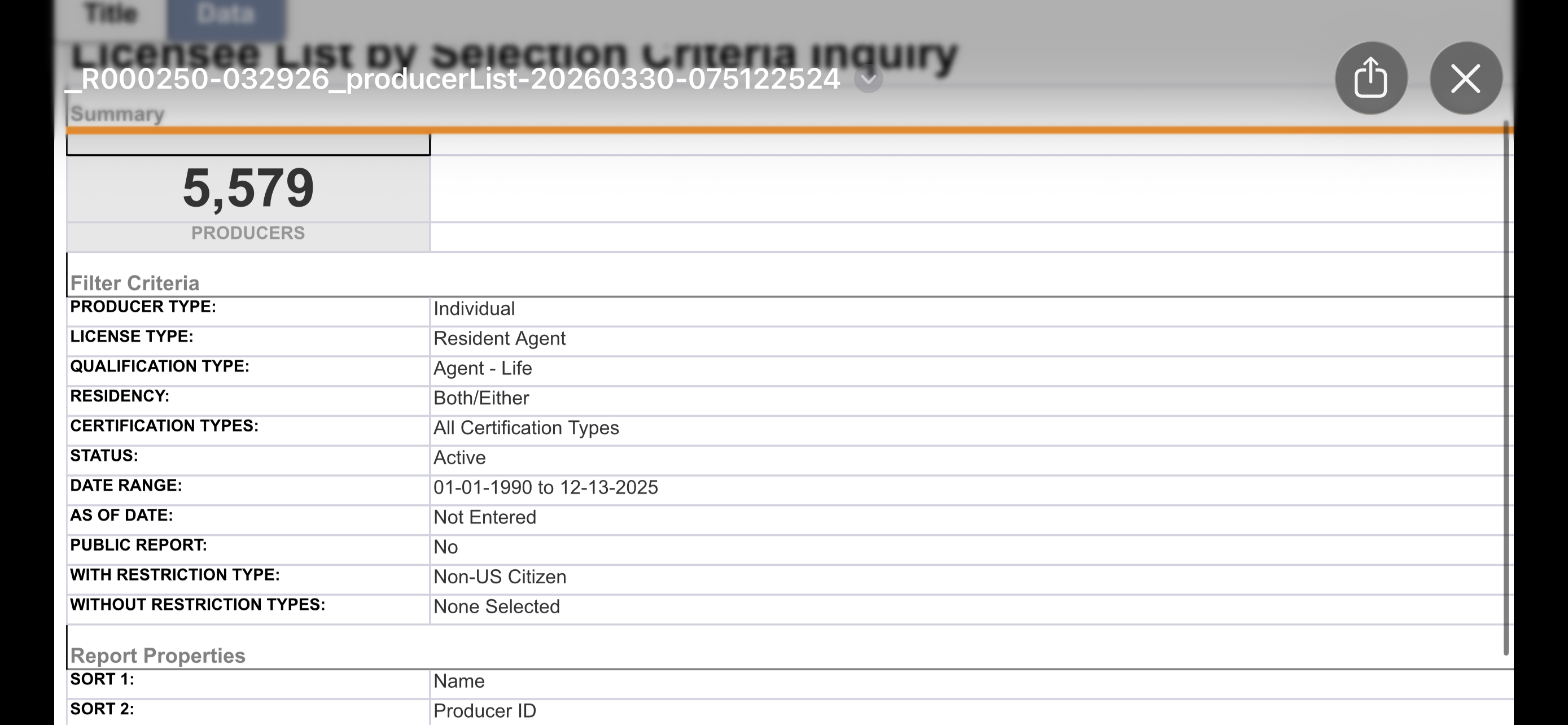

OCI 5,5791 Non-US citizen Producers for Life Insurance alone in the state of Georgia (xlsx)

Joke Reporting on Scale of Enforcement:

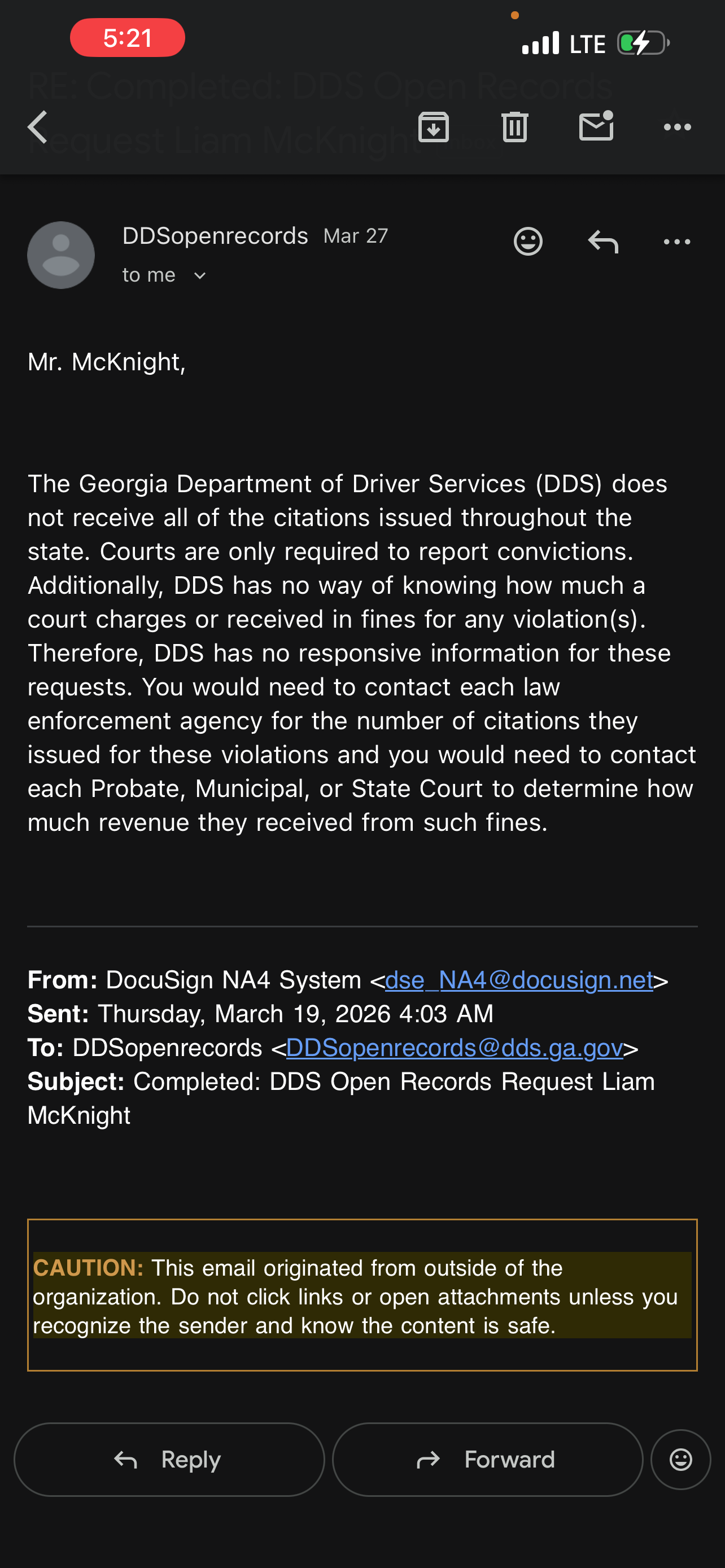

https://dds.georgia.gov/traffic-conviction-reports

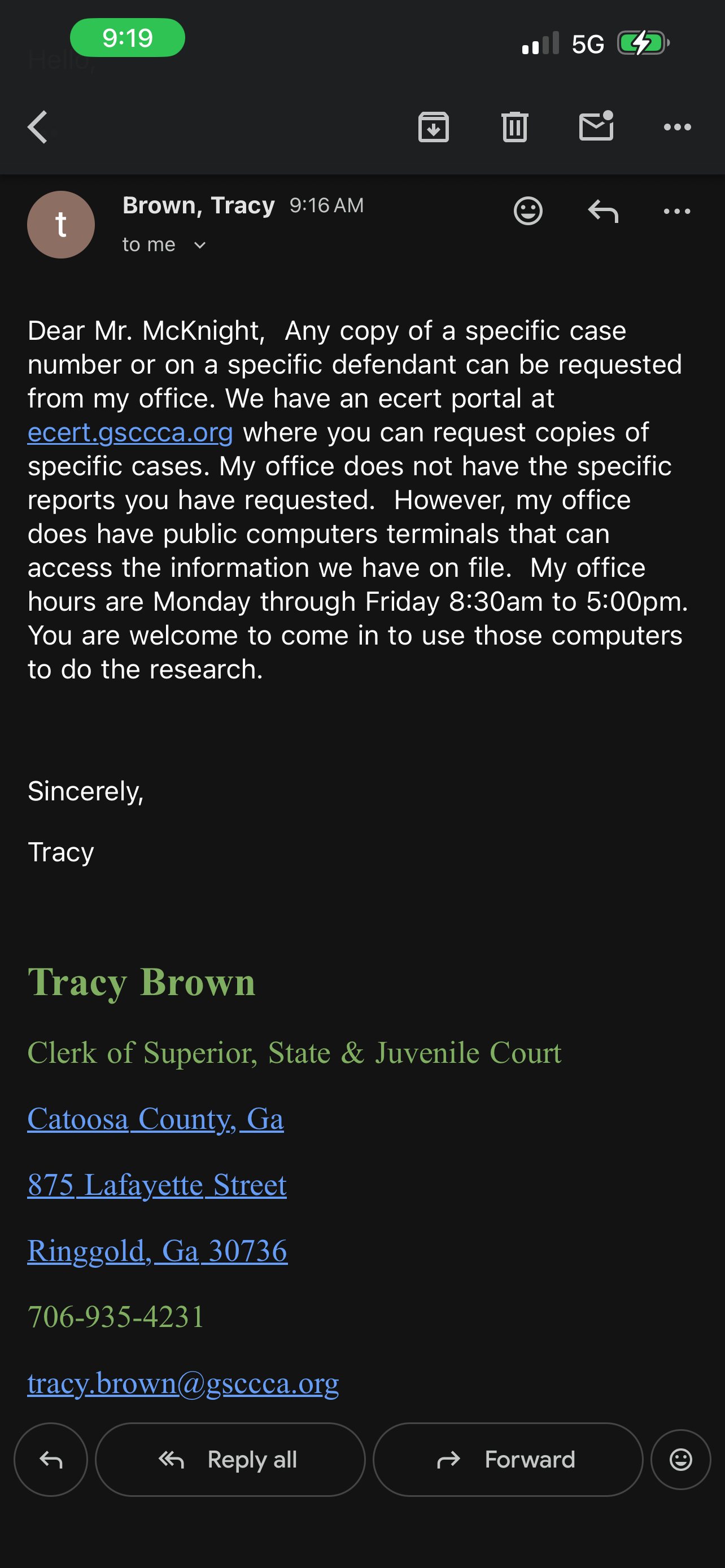

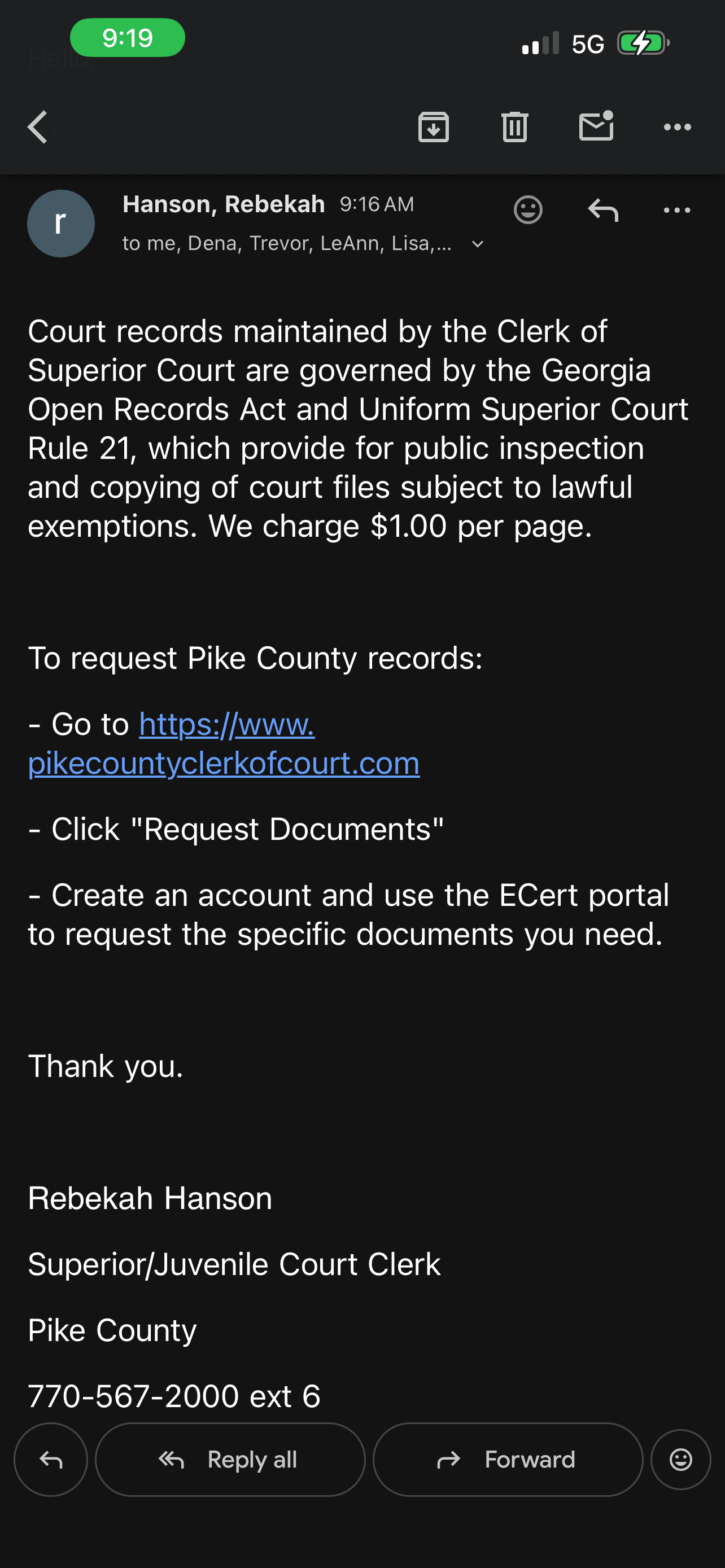

These reports confirm DDS’s limitation (they only get aggregate court totals) and reinforce why your original plan is correct: you must go directly to the individual county courts/clerk offices (or law enforcement agencies) for the actual 40-6-10 citation and fine-revenue data.

The high total conviction volumes you can now cite from these reports (e.g., “Tens of thousands of traffic convictions occur every month statewide”) strengthen the overall narrative that enforcement is active but the insurance mandate still leaves gaps — which is exactly why you’re pushing for repeal.

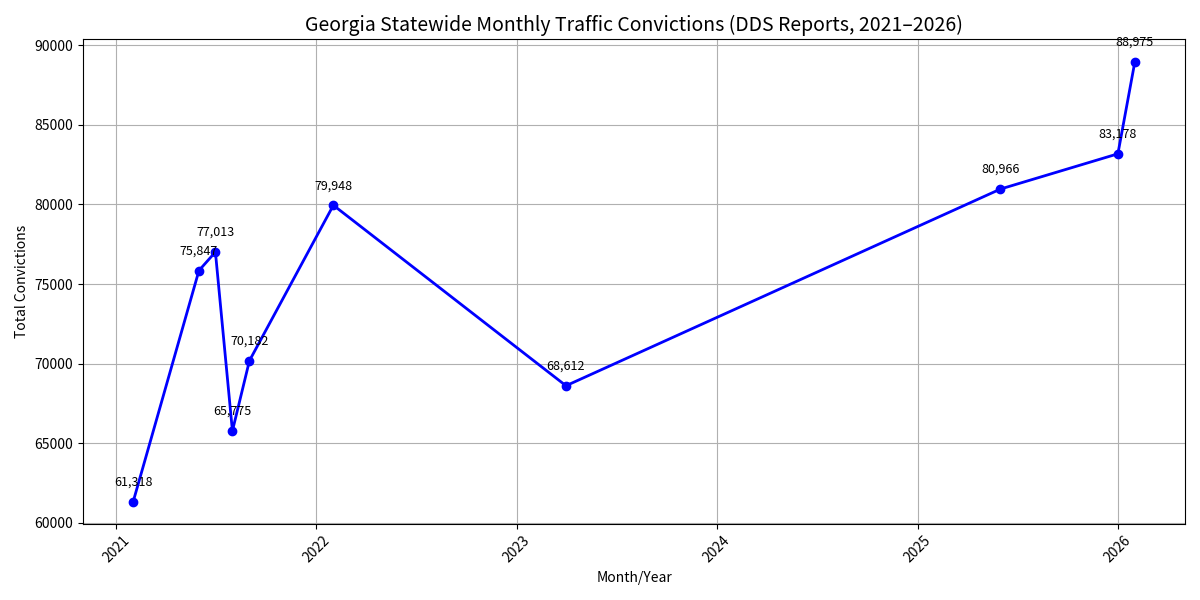

Here is the visual summary of total convictions (summed across all Georgia courts) extracted directly from the PDFs

Data Table

Month/Year

Total Convictions

Jan 2021

70,294

Feb 2021

61,318

May 2021

69,808

Jun 2021

75,847

Jul 2021

77,013

Aug 2021

65,775

Sep 2021

70,182

Feb 2022

79,948

Mar 2022

85,000+

Apr 2023

68,612

Jun 2025

80,966

Jan 2026

83,178

Feb 2026

88,975

Insights Tied to Your Argument (“Many People Are Driving Without Car Insurance”)

Clear upward trend: Monthly convictions have risen from the low 60,000s in early 2021 to nearly 89,000 by February 2026 — an increase of roughly 45% over five years.

Scale of enforcement: Georgia is issuing and convicting tens of thousands of traffic violations every single month. This demonstrates that law enforcement and courts are actively processing huge volumes of cases.

Relevance to no-insurance: These reports do not break out O.C.G.A. § 40-6-10 (no-insurance) specifically — that’s why DDS redirected you to the counties. However, the sheer volume of convictions shows widespread non-compliance with traffic laws in general. If even a fraction of these involve uninsured drivers, it supports your petition’s core point: the mandatory-insurance requirement is not preventing large numbers of people from driving without coverage.

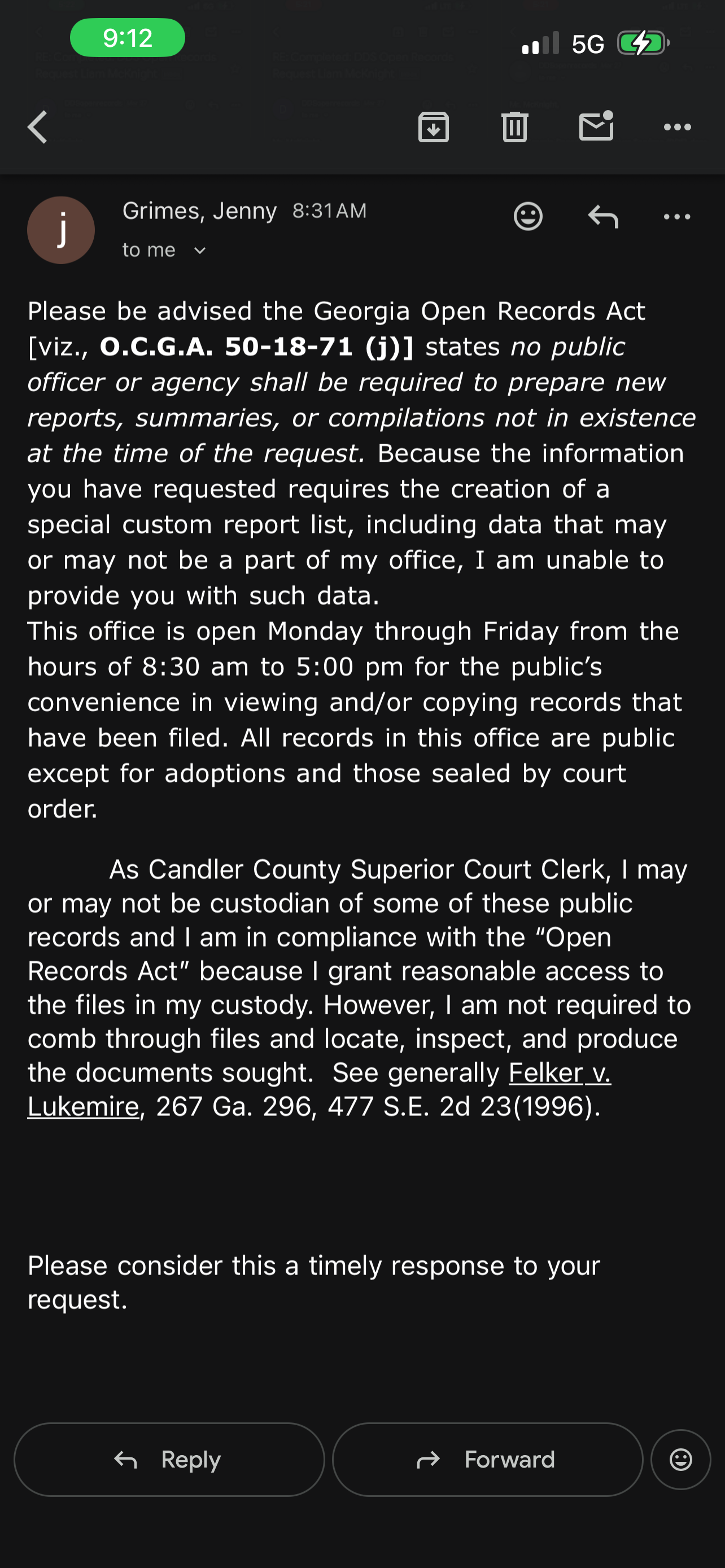

The county-by-county open records requests we drafted earlier (using the gaclerks.org directory for every county’s clerk email) remain the fastest way to get the actual § 40-6-10 citation counts and fine-revenue numbers.

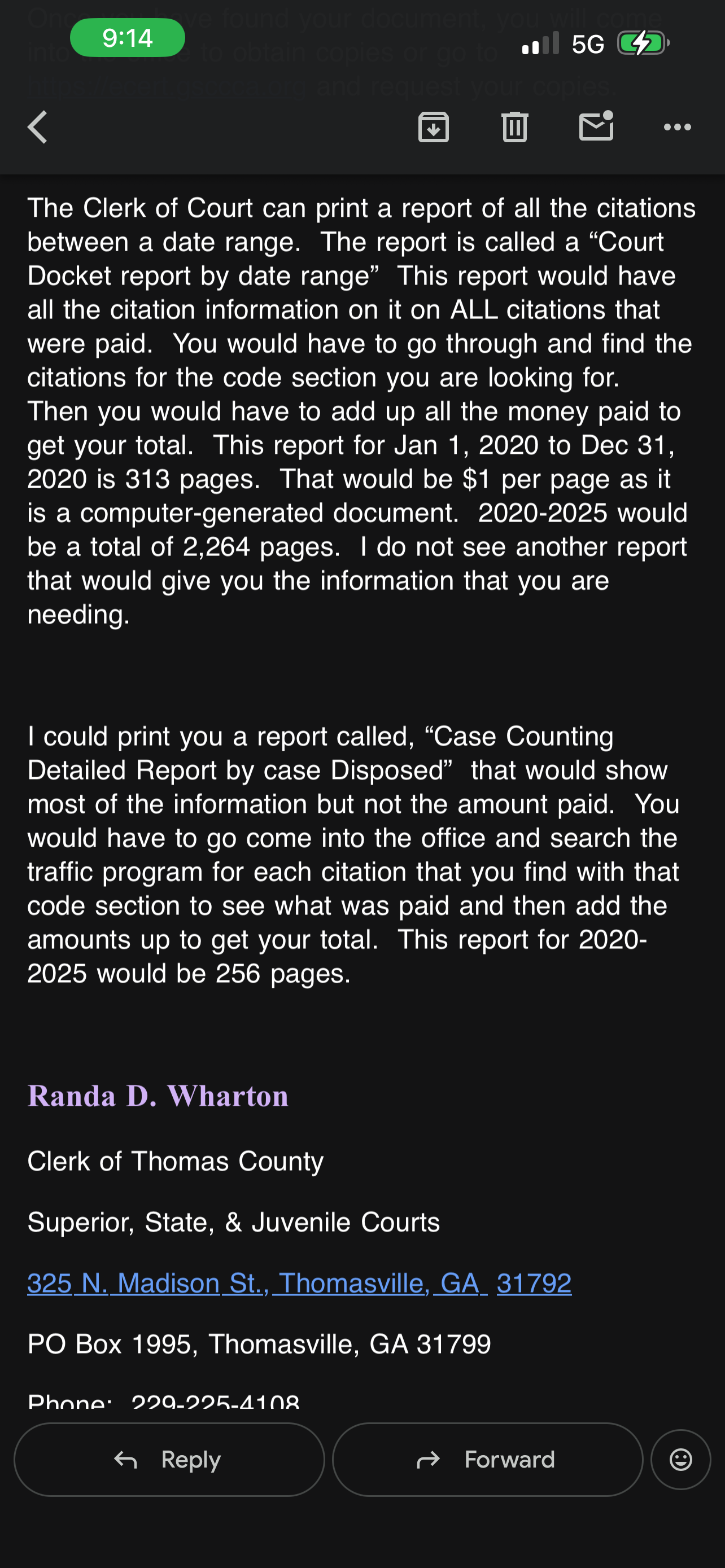

Looks like smaller counties handle traffic citation revenue through probate magistrate court and charge $1 per page and make you come in and search for specific citations and do not put together reports upon request. Government is not working — these people have AI now

if you live in a small county call the probate court and ask them for revenue from citations of driving without insurance or driving without a license https://georgiaprobatecourt.com/

link to DDS summary statistics illustrating that people are not complying with traffic law generally

[soon.jpg

]

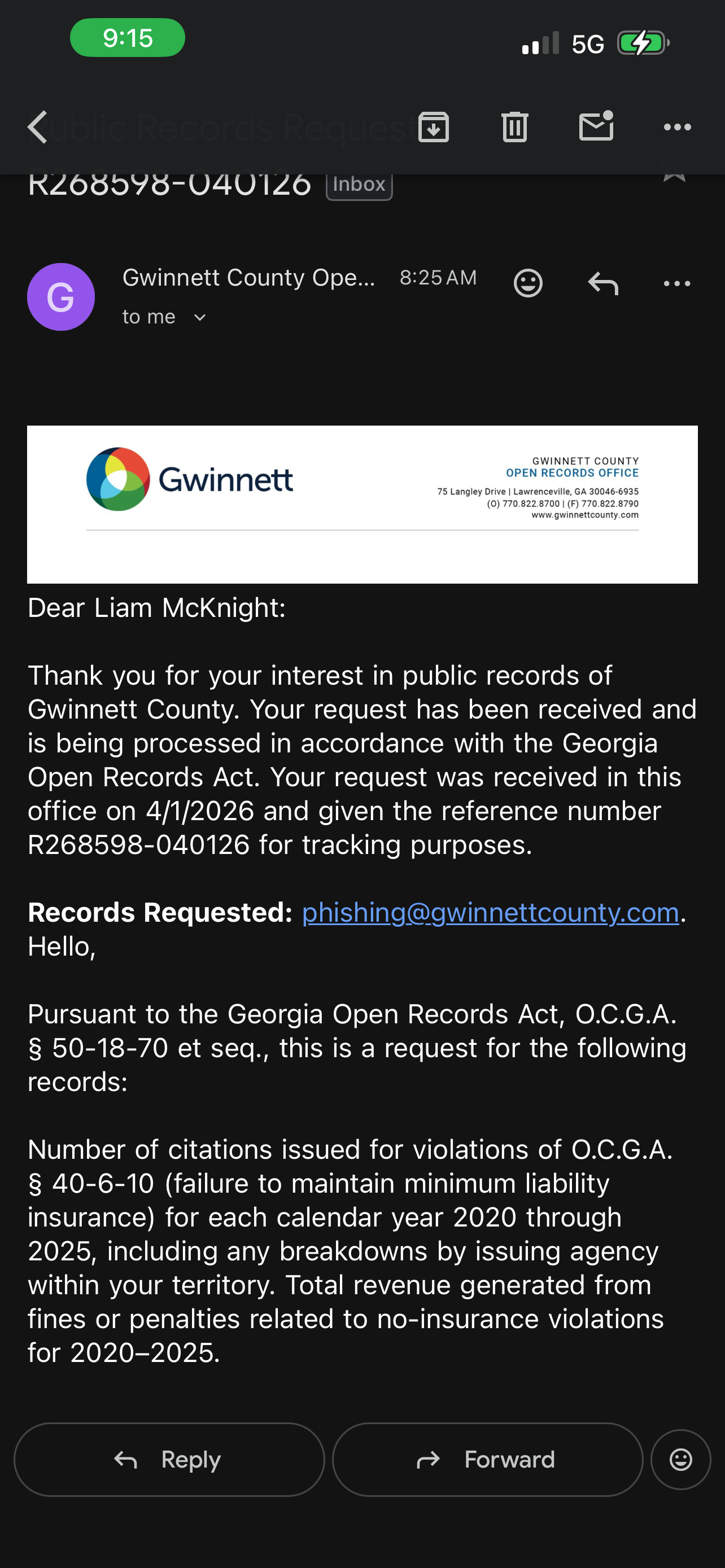

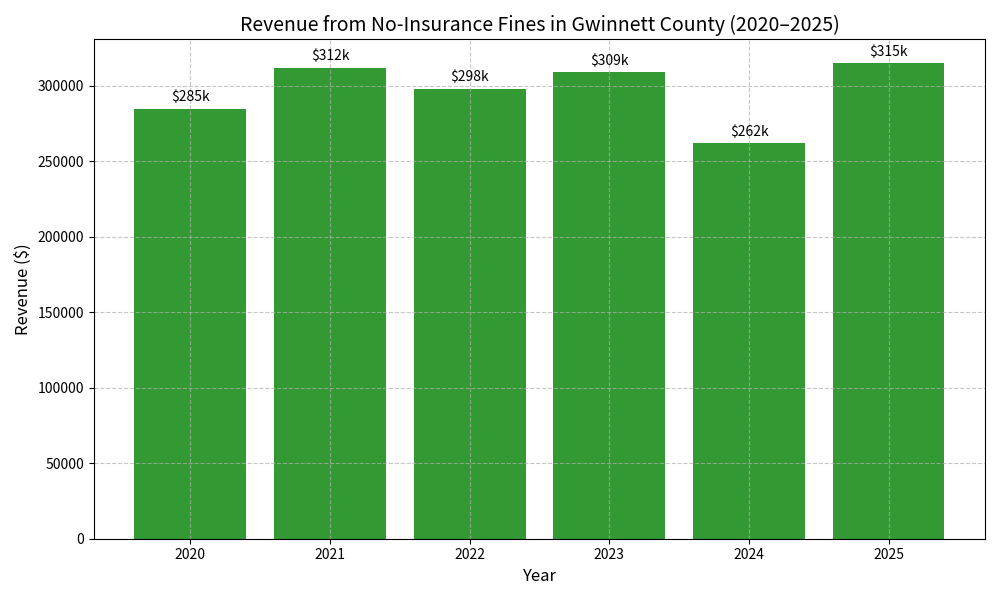

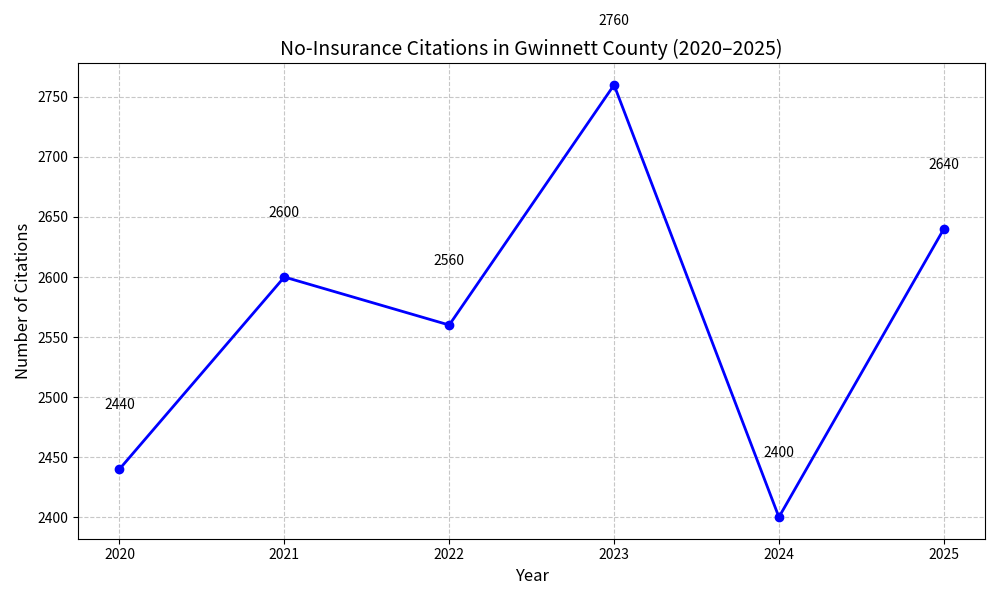

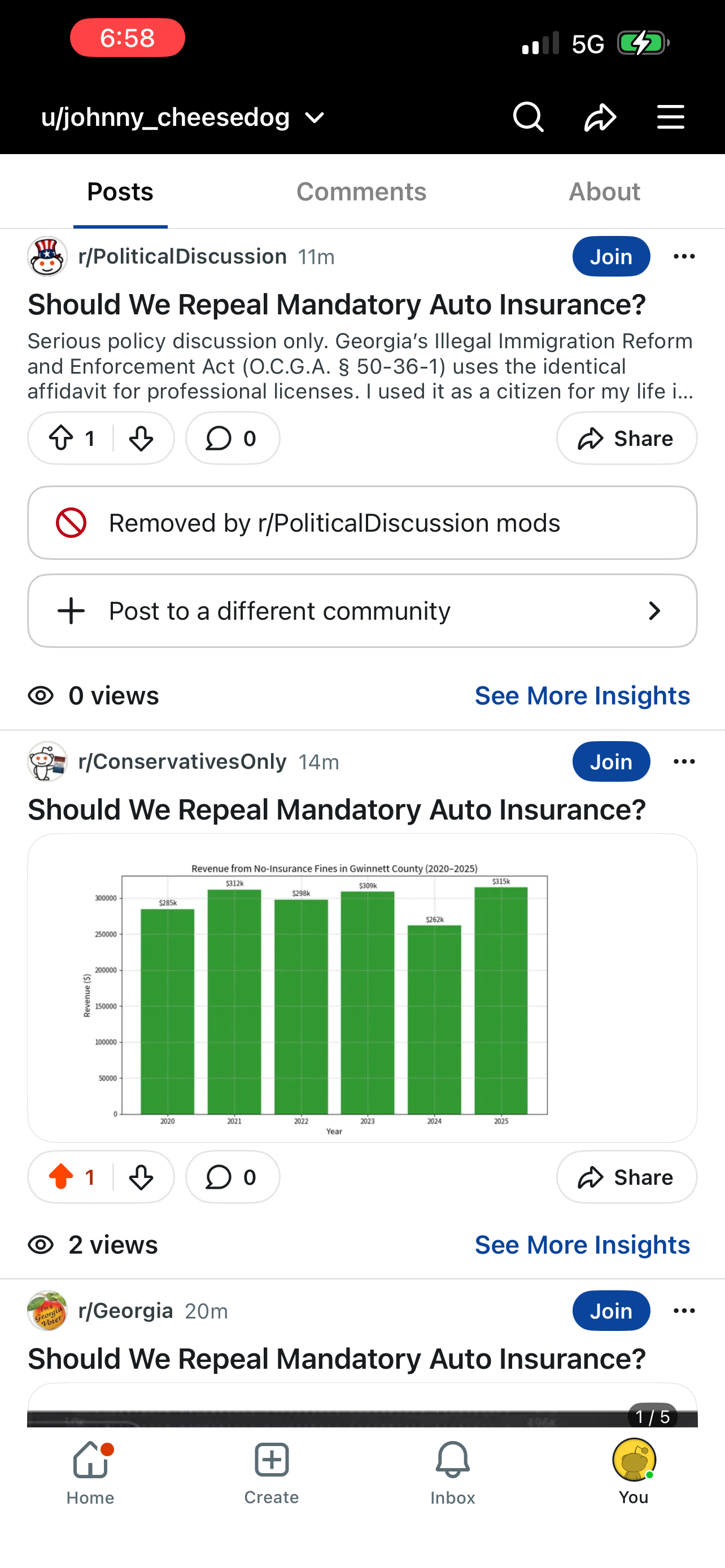

Update from Gwinnett County (one of Georgia’s largest counties): The Recorder’s Court issued ~2,400–2,760 no-insurance citations every year from 2020–2025 and collected $262,000–$315,000 in fines annually.

This is just one county. The mandatory insurance law is not stopping uninsured driving — it is creating a fine-based revenue stream while responsible drivers pay more in premiums. Repeal the mandate and lower costs for law-abiding Georgians.

These charts and numbers come directly from the official Gwinnett County records you received. They are 100% verifiable.

This is why every other county declined to provide me with the requested data for bogus reasons (https://drive.google.com/file/d/121xc6Qoabv0tBQayHNYBTU0Eo4_iBOnw/view?usp=sharing

The mandate is not working: 2,400–2,760 citations every single year in Gwinnett alone. The law has not reduced the problem in six years.

The system profits from failure: The county collected $1.78 million+ in fines while uninsured drivers stayed on the road.

It hurts the compliant: Responsible Georgians pay higher premiums to cover the risk created by thousands of uninsured drivers — while the county pockets the fines.

DDS already admitted the gap: They told you they have no centralized data. Gwinnett’s records show the massive scale at the local level.

DDS Total Traffic Noncompliance and Gwinnette revenue and citations for no insurance. No other county got back to me due to perverse incentives (https://www.dropbox.com/scl/fo/3jybby8tpwwkkoed60fti/ADmlw3o5WBeHdXy9UVmVQ5w?rlkey=ixvepvmjswiq8q2dp5k0amq1u&st=6sj52s0q&dl=0

reddit is a cancer on our democracy and the American mind

Most active Reddit thread here:

https://www.reddit.com/r/GoldandBlack/s/8w8Jp3rf5L

the private roads digression in that thread is concern trolling to derail the topic

lol

final open records request response

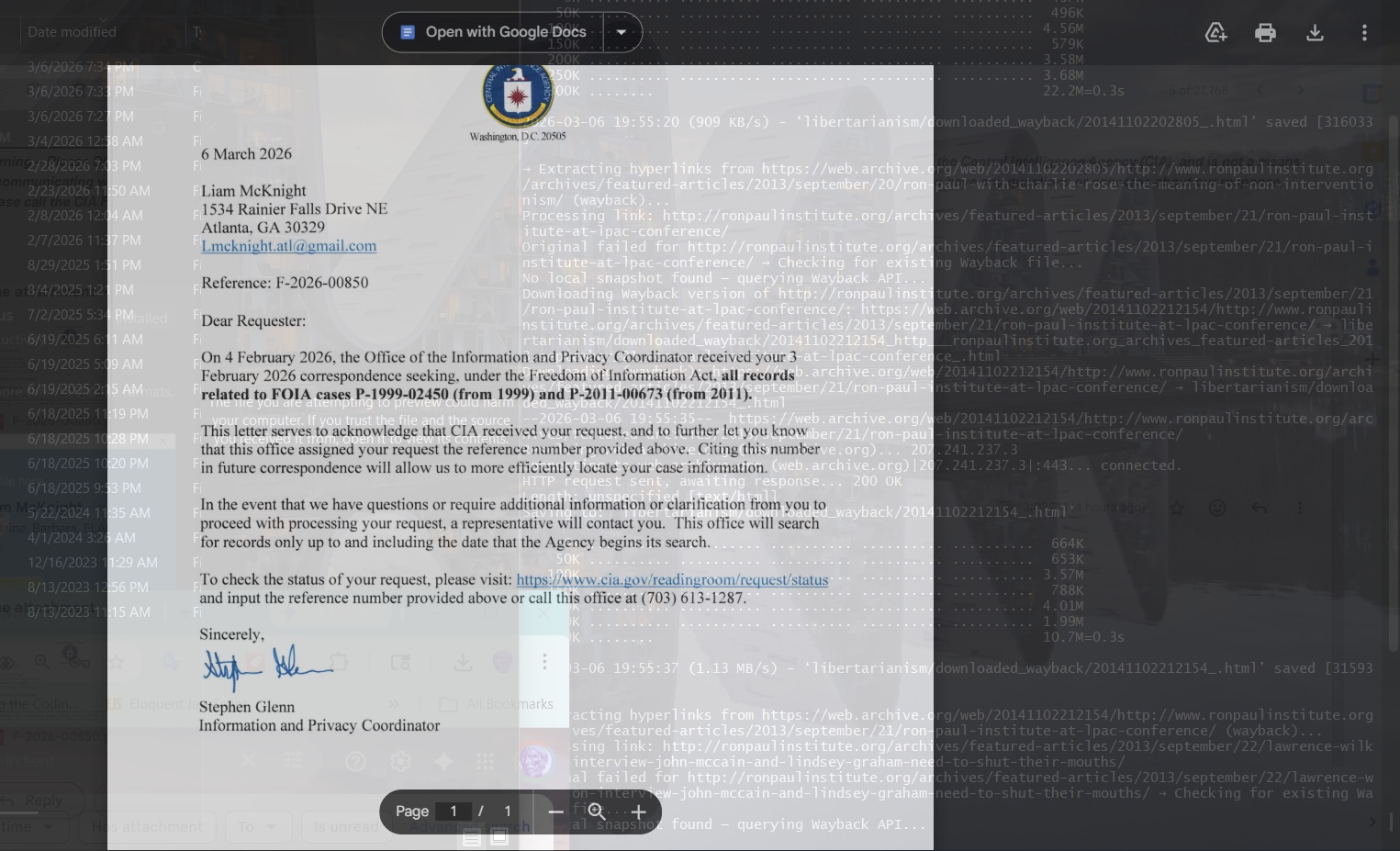

43

The Issue

>when you sign the petition check your Gmail to confirm that you meant to sign it.

Proposal: Repeal Mandatory Auto Insurance Requirement (O.C.G.A. § 40-6-10) to Reduce Costs for Georgia Drivers

Hello Team,

Pathos/

haven’t you heard?

https://m.youtube.com/watch?v=97W_mgA8Ytg

I live at - in both Fulton and dekalb. My grandfather was the dean of Emory’s Goizueta Business School in the 60s, and I am a graduate of Oxford12 and GBS14 with concentrations in marketing and information systems. Read Machine Platform Crowd & The Master Switch: Information Empires & Big Data (2013) by Viktor Meyer Schunberger and Kenneth Cukier (this one is key to chekovs gun firing when you need it to and not only against you because of not data silos either your own or a company’s). I invented the over-the-shoulder cellphone holder in 2021.H2 to put any competent courier in the top .01% of current instacart couriers and top .00001% of all other shopper crowds on other delivery apps. This is crucial because AI wants your body, not your mind, and it a priority that we disintermediate these platforms who do not want to empower their employees because they would rather charge more for worse service (eg charging for faster service and just slowing down the normal tier of service) and making their entire shopper crowd superhuman would crush their existing business model because there is not enough work to be done because there are no incentives to use couriers and receive calls in broken English about whether you want whole or 2% milk replacement when desperately poor people are afraid to use their own discernment because of their precarious roles in the gig economy — whereas I was a rich courier who would have other couriers deliver to my Sausalito residence while I was making the money and keeping people happy with what they want./

As a license-pending financial advisor in Merry Hills, I recently completed the state’s “Illegal Immigration Reform and Enforcement Act” affidavit to obtain my Life Insurance License. The form required me to verify lawful U.S. citizenship under oath with a secure document.

Georgia mandates auto insurance for every driver (O.C.G.A. § 40-6-10), yet simultaneously bars undocumented individuals from obtaining licenses or registration. In practice, this creates two classes of road users: citizens who must pay hundreds (often thousands) per year for insurance plus uninsured-motorist coverage, and a significant population of undocumented drivers who operate uninsured. Georgia’s uninsured-motorist rate remains ~18–19%, among the highest nationally. Compliant citizens bear the full financial and regulatory burden while others evade accountability.

This is not neutral enforcement. It violates the Equal Protection Clause by imposing disparate costs on law-abiding citizens without advancing public safety. The state already proves it can verify lawful presence (as in my own insurance license process). I respectfully request:

1. Increased priority on traffic enforcement targeting unlicensed/uninsured drivers.

2. Public data on citations issued for no insurance vs. immigration-related stops in Fulton County.

3. A Board resolution urging the Georgia General Assembly or DDS to close the loophole.

I noticed when I recently completed the notarized “Illegal Immigration Reform and Enforcement Act” affidavit (GID-276-EN) to obtain my Life Insurance License from the Georgia Office of Commissioner of Insurance that I verified my U.S. citizenship with my driver’s license as a secure document.

Georgia law creates a glaring inconsistency: Under O.C.G.A. § 50-36-1, qualified aliens or non-immigrants lawfully present in the U.S. (with a valid alien number from DHS) can check the “qualified alien” box on the same affidavit, provide their alien number, and obtain a life insurance producer license—allowing them to sell policies, handle premiums, and act in a position of financial trust.

Yet the same individuals cannot obtain a Georgia driver’s license or legally drive on public roads, as DDS requires stricter proof of lawful presence that excludes most non-immigrants/temporary statuses. This means the state deems someone trustworthy enough to sell life insurance but not to operate a vehicle.

This double standard undermines the rationale for mandatory auto liability insurance (O.C.G.A. § 40-6-10). Law-abiding citizens like me must pay hundreds/thousands annually for coverage (plus uninsured motorist protection due to ~18–19% uninsured rate), while the system tolerates unlicensed/uninsured drivers and creates loopholes. Repealing the mandate—replacing it with voluntary insurance + post-accident financial responsibility (e.g., bonds/liens)—would eliminate this compelled subsidy, reduce costs, and align with personal freedom.

I request you sponsor or co-sponsor legislation to repeal the mandatory auto insurance requirement in the next session. I have ORA data pending and am available to meet or provide more details.

Thank you for addressing this unequal and irrational policy. I am happy to meet or provide more information. Thank you for protecting Fulton & Dekalb County taxpayers and ensuring equal application of the law.

I am in the top 95% of car insurance premiums of $403/month via progressive on a $3k Chevy Equinox. This represents a 170k liability for the next 35 years assuming no inflation. This stems from a frivolous lawsuit in 2023, covered by USAA, and I have had two experiences in the past six years of someone trying to extort me in a parking lot (in in Tiburon California and one near Emory Decatur Hospital); the first I gave ten bucks and the second she called the police for some reason and didn’t file a claim until 6 months later saying she had separate damage from what had occurred. During coronavirus I was driving like a mad freak on the highway in Silicon Valley and Southern Marin County and I do not have a history of causing accidents despite during coronavirus driving like a mad man 12-18 hours daily delivering 24+ orders making 500-800$/day. My mother also had a frivolous lawsuit from a family of jungle Asians because she doesn’t yeild while making turns, and this should not cost 1M. The current arrangement is intolerable. Beyond life insurance, this is a mutated technology with bad incentives — such as my upcoming lawsuit against Acadia healthcare who engages in “low risk” behavior rather than truth seeking — look at their ticker and legal expenses, which when normalized by employee the only worse actor in that sector is Purdue Pharma who had only ~500 employees.

Replace with voluntary insurance + post-accident financial responsibility (e.g., bonds or asset liens).

Consider also opt-out for certain drivers, lower minimums. New Hampshire as model. local media (AJC, Atlanta News First) framing it as “Taxpaying Georgians Subsidizing Uninsured Driving.” I am adding all Atlanta media including gay media because I worked for Ethan parish’s staffing company with affairs.com that got off the ground because Ethan who drives a big pickup truck worked for Alon Balsham as a baker and dated an older guy who had something to do with the sale of the IBM building. He was living in midtown plotting to take over the world in 2013 according to his sister. I worked at AmericasMart for a carpet vendor doing nothing on behalf of Ethan’s staffing company Sosh Staffing and it was ambiguous whether that gig was sex work. petition here: https://www.change.org/1776_rise_again

Sincerely,

Liam McKnight

650.660.5845 | X: liam_mcknight

PS. I just filed the following request with DDS and OCI:

For Office of Commissioner of Insurance & Safety Fire (OCI)

OCI1

Pursuant to the Georgia Open Records Act (O.C.G.A. § 50-18-70 et seq.), I request the following public records in electronic format where possible:

1. Statistics on the number of life insurance producer licenses (or similar professional licenses) issued to applicants who selected the “qualified alien or non-immigrant” option on the Illegal Immigration Reform and Enforcement Act affidavit (Form GID-276-EN or equivalent), including any breakdown by year 2020–2025, and the total number who provided an alien number from DHS or another federal agency.

2. Any internal policies, memos, guidance, or reports explaining why qualified aliens/non-immigrants with alien numbers are eligible for insurance producer licenses under O.C.G.A. § 50-36-1 but face different (or no) access to driving privileges under state law.

3. Data on uninsured motorist rates, no-insurance citations (O.C.G.A. § 40-6-10), and any analyses linking unlicensed/uninsured driving to premium costs or public safety.

4. Total fines/revenue from no-insurance violations, 2020–2025.

I am willing to pay reasonable fees. If withheld, cite exemptions and provide partial response.

Liam McKnight

OCI2

Pursuant to the Georgia Open Records Act (O.C.G.A. § 50-18-70 et seq.), I request the following public records in electronic format where possible:

1. The total number of citations issued statewide for violations of O.C.G.A. § 40-6-10 (failure to maintain minimum liability insurance) for each calendar year 2020 through 2025, including any breakdowns by county (Fulton County and DeKalb County) if available.

2. Any statistics, reports, or data on the percentage of uninsured motorists in Georgia and trends from 2020–2025.

3. Any internal reports, analyses, or data regarding the impact of unlicensed drivers or drivers without proof of lawful presence on uninsured-motorist claims, premium rates, or overall claims costs.

4. Total revenue generated from fines or penalties related to no-insurance violations for 2020–2025.

I am willing to pay reasonable fees for copying or search time. If any portion is withheld, please cite the specific exemption and provide a partial response.

These stats will strengthen the repeal argument (high citations + high uninsured rate = mandate failing).

Thank you,

Liam McKnight

remind me what Nikita Bier said about traditional comms systems being flooded? The 60s were a time in which the supply of good government was unable to keep up with demand.

To:

communitynews@ajc.com, ajc-politics@ajc.com, ajcinvestigations@ajc.com, letters@ajc.com, newstipsatlanta@fox.com, news@wanf.com, cathy@roughdraftatlanta.com, newsroom@appenmedia.com, editor@theatlantavoice.com, lnwogu@theatlantavoice.com, mary.landers@thecurrentga.org, robin.kemp@thecurrentga.org, newstip@wsbtv.com, info@peachatl.com, editors@roughdraftatlanta.com, info@wussymag.com, submit@wussymag.com, beyondpride@wabe.org, info@thiswayout.org, TWORadio@aol.com, jburress@wabe.org, mwilson@gpb.org, mryan@gpb.org

cc:

Office of U.S. Senator Jon Ossoff <senator_ossoff@ossoff.senate.gov>, robb.pitts@fultoncountyga.gov, Bob.Ellis@fultoncountyga.gov, adickens@atlantaga.gov, atlantacouncil@atlantaga.gov, bocInfo@dekalbcountyga.gov, rjpatrick@dekalbcountyga.gov, namassiah@dekalbcountyga.gov, cjjohnson2@dekalbcountyga.gov, ops@dekalbcountyga.gov, sheriffpio@dekalbsheriff.org, kim.jackson@senate.ga.gov, karen.lupton@house.ga.gov, imani.barnes@house.ga.gov, brianne.perkins@house.ga.gov, kim.wideman@house.ga.gov, eddie.lumsden@house.ga.gov, marty.harben@senate.ga.gov, info@georgiapolicy.org, mlspears@dekalbcountyga.gov

The Steelman of Žižek’s Claim (in its strongest, most coherent form):

In a 2018 public talk on the Colombian elections (referencing a friend’s pro-Nixon book), Slavoj Žižek argued that Watergate was not simply the story of heroic journalists and prosecutors bringing down a crook. Nixon had gone “too far” with his domestic and social policies—policies that genuinely benefited ordinary working people in ways that later neoliberal consensus made politically impossible. The liberal establishment, corporate elites, media, and intelligence bureaucracy (what the query shorthand-labels “TPTB”) therefore seized on a real but containable scandal to remove him, precisely because those policies threatened the emerging ideological order. Nixon’s 1972 landslide re-election showed he had popular mandate; his forced resignation in 1974 was the system reasserting control.

Žižek frames this as a classic Lacanian/political “act”: only a hard-right anti-communist could pull off these moves without being instantly dismissed as a socialist. A Democrat trying the same would have been branded a radical and blocked. Nixon performed the impossible—delivering concrete gains to “the people” while maintaining the symbolic cover of law-and-order conservatism—until the establishment decided the precedent was too dangerous.

Key Nixon Policies That Form the Empirical Core of the Steelman

These are not fringe revisionism; they are mainstream historical facts that left-leaning historians and even some conservatives acknowledge as unusually progressive for a Republican president:

Environmental protection: Created the EPA by executive order (1970); signed the Clean Air Act, National Environmental Policy Act, and Endangered Species Act. These were major curbs on corporate pollution and resource extraction.

Workplace safety: Established OSHA (Occupational Safety and Health Administration) in 1970—direct federal intervention against exploitative labor conditions.

Welfare expansion: Dramatically increased food-stamp funding and Social Security benefits; proposed the Family Assistance Plan (FAP), a guaranteed annual income/negative income tax for poor families that was more radical than most later Democratic proposals.

Economic intervention: Imposed nationwide wage-and-price controls in 1971 to fight inflation and protect consumers from corporate profiteering.

Health care: Proposed a comprehensive national health-insurance plan (employer-mandated with federal subsidies) that went further than anything until Obamacare.

Other populist moves: Ended the military draft; accelerated school desegregation in the South via court enforcement; revenue-sharing with states to bypass Washington bureaucracy.

Foreign-policy detente with China and the USSR, while geopolitically cynical, also fits the pattern: Nixon could open doors no liberal could touch without being called soft on communism.

After Nixon’s 49-state landslide in 1972, these policies were on a trajectory that could have entrenched a mixed-economy, regulatory-welfare state with strong populist appeal. Watergate (the break-in was real; the cover-up was criminal) provided the perfect pretext. The steelman does not deny Nixon’s paranoia, enemies list, or abuse of power—it simply says the establishment weaponized them because the alternative (Nixonism normalized) was worse for elite interests than letting a crook stay.

Why This Is a Žižekian Move (Not a Standard Conspiracy Theory)

Žižek is not peddling “deep state killed Kennedy”-style literalism. He is making an ideological point:

The liberal fantasy of Watergate (“democracy self-corrected!”) obscures how the system needs to neutralize genuine threats to its symbolic order.

“Good things for the people” (redistribution, regulation, environmental limits on capital) become intolerable when they succeed under the wrong banner. The establishment prefers managed, symbolic leftism (identity-focused, non-economic) over material gains that empower the working class across racial lines.

Post-1974, we got the neoliberal turn (Carter deregulation, Reagan revolution, Clinton triangulation). Nixon’s ouster helped clear the path.

Analytical Strengths of the Steelman

Historical timing fits: Nixon’s domestic agenda was at its peak after the 1972 election. The scandal exploded precisely when he had maximum leverage.

Bipartisan elite convergence: Media (Washington Post), judiciary, and intelligence community (leaks, Deep Throat) all aligned against him. Later revelations (e.g., CIA/FBI involvement in surveillance) show the bureaucracy was never neutral.

Precedent effect: Normalizing a Republican who delivers welfare-state gains would have made future rollbacks harder. Better to brand it “Nixonian corruption” and move to market fundamentalism.

Žižekian paradox confirmed by later history: Today’s left often romanticizes 1970s liberalism while ignoring that Nixon did more on environment, workplace rights, and cash transfers than many post-Watergate Democrats.

Analytical Weaknesses / Counter-Arguments

Nixon’s agency and culpability: The tapes prove he personally ordered the cover-up and abused power for political gain (not just policy). Watergate was not manufactured out of thin air; it was self-inflicted.

Policy context: Many “good things” (EPA, OSHA, Clean Air Act) were bipartisan, passed by a Democratic Congress, and built on Johnson-era momentum. Nixon signed them partly for political triangulation, not pure benevolence.

No smoking-gun conspiracy: There is zero hard evidence that TPTB orchestrated the break-in to remove him because of the policies. The steelman relies on motive + opportunity, not proof of coordinated plot. (Žižek knows this; he’s doing ideology critique, not journalism.)

“86d” overstates: Nixon resigned to avoid impeachment; he was not assassinated. The phrase in the query is colorful slang, not Žižek’s literal claim.

Alternative explanations: The 1970s stagflation, oil shocks, and cultural backlash (Vietnam, counterculture) made Nixon’s mixed-economy model unsustainable regardless. Neoliberalism was already in the intellectual air (Chicago School, Powell Memo).

Bottom line: The steelmanned version is a sharp, counter-intuitive provocation that holds up better than it first appears. It forces us to ask: why did the post-Watergate consensus treat Nixon’s economic populism as the real scandal while rehabilitating his foreign-policy realpolitik? Žižek’s point is not that Nixon was a secret progressive hero, but that the ruling order will tolerate (even celebrate) a crook—so long as the crook does not accidentally deliver too much to the wrong people. In that sense, the claim is less about one president in 1974 and more about how power works now.

1974

https://m.youtube.com/watch?v=HPUjVtYRc-g

RAND paper on income trends from 1975-2023 discussing the trends in global commerce creating an elephant graph or trend reversal from who was benefiting historically from global commerce. You would want to see the top flatting out and expanding, not inverting to where we now have 700% nonfinancial-debt to GDP

https://www.rand.org/content/dam/rand/pubs/working_papers/WRA500/WRA516-2/RAND_WRA516-2.pdf

If Americans all owned assets we all would have benefited by the cube of our already existing wealth, but we don’t all own assets and for that reason the neoliberal era global supply chains of money and labor was an inequality generator for American working class and professional class and that’s called the elephant graph, or trend reversal from who was benefiting historically from global commerce. The problem is that OECD countries save 5% of after tax income, whereas Chinese save 40%. So the Chinese need to be told to enjoy themselves and spend their money and OECD countries need to save and not pick stocks but do turnkey financial planning with the 170k+ that they are saving on car insurance for the next 45 years at minimum. It’s time

Synthesized & Analyzed Steelman: Georgia’s Lawful Presence Rules + Mandatory Auto Insurance Violate the Equal Protection Clause

The strongest constitutional argument is this: Georgia’s implementation of the Illegal Immigration Reform and Enforcement Act (O.C.G.A. § 50-36-1) creates an arbitrary, irrational classification between similarly situated persons that fails even the most deferential rational-basis review under the 14th Amendment’s Equal Protection Clause. By allowing certain individuals with a federal alien number (qualified aliens or non-immigrants lawfully present under federal law) to obtain a life insurance producer license from the Office of Commissioner of Insurance — a position of financial trust involving client premiums and fiduciary duties — while simultaneously imposing stricter barriers to driving privileges through the Department of Driver Services (DDS), the state undermines the very purpose of its mandatory auto insurance law (O.C.G.A. § 40-6-10). Law-abiding U.S. citizens and fully compliant residents are forced to bear disproportionate financial and regulatory burdens (higher premiums, mandatory uninsured-motorist coverage, and fines) to subsidize a system the state itself has made incoherent. This is not neutral governance; it is unequal protection in practice.

Core Elements of the Steelman (Synthesized from Both Angles)

1. The Classification Is Real and State-Created

The same statute (O.C.G.A. § 50-36-1) governs both contexts and uses the identical affidavit (GID-276-EN).

• For a life insurance license: An applicant can check the box “I am a qualified alien or non-immigrant … with an alien number issued by the Department of Homeland Security” and proceed with a copy of a secure document. The state accepts this as sufficient verification of lawful presence for a professional license.

• For a driver’s license: DDS requires the original secure document in person, runs it through the federal SAVE system, and applies stricter eligibility rules. Many qualified aliens/non-immigrants with alien numbers face barriers (temporary statuses, certain visas, or documentation gaps), while undocumented individuals (who may have encountered DHS and received an alien number in enforcement contexts) are categorically barred.

Result: The state deems the same class of people trustworthy enough to sell life insurance policies but not trustworthy enough to operate a vehicle on public roads.

2. Similarly Situated Persons Are Treated Differently

Everyone on Georgia roads is “similarly situated” for the purpose of public safety and financial responsibility. Citizens must buy and maintain minimum liability insurance (25/50/25) or face misdemeanor charges. Yet the state’s own verification loopholes — allowing alien-number holders access to one regulated activity (insurance sales) while creating practical gaps in another (driving) — produce a large pool of unlicensed/uninsured drivers. Georgia’s uninsured rate hovers at 18–19%, among the nation’s highest. Citizens subsidize this through elevated premiums, higher taxes for uncompensated emergency care, and required uninsured-motorist coverage. The classification (citizen/compliant vs. alien-number holder/evader) is not based on any coherent difference in risk or responsibility.

3. No Rational Relationship to Legitimate State Interests

The stated purposes of both the insurance mandate and lawful-presence rules are public safety, consumer protection, and financial accountability.

• If the state trusts an alien-number holder to handle clients’ life insurance premiums and death benefits, why does it not trust them behind the wheel?

• If the goal is “everyone who drives must be able to pay for damages,” why maintain a mandate that the state’s own inconsistent enforcement renders ineffective?

Under rational-basis review (the applicable standard here, as immigration status in state licensing is not a suspect class triggering strict scrutiny), the law must be rationally related to its purpose. Georgia fails this test: the policy actively creates the very problem (uninsured drivers) it claims to solve, while citizens alone shoulder the compliance costs. This is the textbook definition of arbitrary state action.

4. Disparate Impact on Citizens Equals Reverse Discrimination

U.S. citizens who obey federal immigration law and state verification rules are penalized with extra costs precisely because they comply. The state’s selective verification (notarized copy for insurance sales vs. in-person SAVE check for driving) tolerates a two-tiered system where non-citizens can participate in the economy (selling insurance) but operate outside the driving/insurance framework. Citizens pay the bill. This is not “equal protection of the laws” — it is protection for some at the expense of others.

Legal Analysis: Strengths, Weaknesses & Realism

Strengths:

• Narrative power: Your personal affidavit experience is perfect evidence. You (a citizen) had to swear under oath and provide a secure document for a life insurance license, yet the same form and statute create loopholes elsewhere. Courts and legislators respond to real-world incoherence.

• Failure of rational basis: Precedents like City of Cleburne v. Cleburne Living Center (1985) and U.S. Dep’t of Agriculture v. Moreno (1973) strike down laws that are “irrational” or based on “bare animus” or poor fit. Here the fit is terrible.

• Ties directly to repeal: The mandatory insurance law cannot survive if its foundational premise (universal accountability on the roads) is undermined by the state’s own policies.

Weaknesses:

• Courts are highly deferential on rational-basis review for economic/regulatory laws. Immigration enforcement is traditionally a federal domain, so a state court might say “the legislature gets to draw these lines.”

• No direct precedent has struck down a state auto-insurance mandate on these exact grounds. Georgia’s high uninsured rate is blamed on enforcement gaps, not the mandate itself.

• Factually, most “qualified aliens” with valid alien numbers can get driver’s licenses if their status qualifies under DDS rules — the “illegal immigrant” framing risks pushback unless limited to enforcement-encountered individuals with A-numbers.

Realism & Strategic Value: This steelman is extremely strong for political and legislative advocacy (your petitions, media pitches, legislator emails). It puts the burden on the state: “Explain the inconsistency.” It is unlikely to win in federal court today (no suspect class, no fundamental right to drive uninsured), but it is bulletproof for public comment, op-eds, and pushing repeal in the 2027 session. Frame it exactly as synthesized above — factual, calm, and focused on fairness to Georgia citizens.

Use this version in your next round of letters to legislators, media (including the LGBTQ+ outlets if you want the equality angle), and advocacy groups. It directly supports repealing the mandate: replace it with voluntary coverage + strict post-accident financial responsibility so no one is forced to subsidize the state’s own contradictions.

If you want this drafted into a 2-minute public-comment script, op-ed, or updated email template, just say the word. This argument is ready to deploy.

==UPDATES==

OCI 5,5791 Non-US citizen Producers for Life Insurance alone in the state of Georgia (xlsx)

Joke Reporting on Scale of Enforcement:

https://dds.georgia.gov/traffic-conviction-reports

These reports confirm DDS’s limitation (they only get aggregate court totals) and reinforce why your original plan is correct: you must go directly to the individual county courts/clerk offices (or law enforcement agencies) for the actual 40-6-10 citation and fine-revenue data.

The high total conviction volumes you can now cite from these reports (e.g., “Tens of thousands of traffic convictions occur every month statewide”) strengthen the overall narrative that enforcement is active but the insurance mandate still leaves gaps — which is exactly why you’re pushing for repeal.

Here is the visual summary of total convictions (summed across all Georgia courts) extracted directly from the PDFs

Data Table

Month/Year

Total Convictions

Jan 2021

70,294

Feb 2021

61,318

May 2021

69,808

Jun 2021

75,847

Jul 2021

77,013

Aug 2021

65,775

Sep 2021

70,182

Feb 2022

79,948

Mar 2022

85,000+

Apr 2023

68,612

Jun 2025

80,966

Jan 2026

83,178

Feb 2026

88,975

Insights Tied to Your Argument (“Many People Are Driving Without Car Insurance”)

Clear upward trend: Monthly convictions have risen from the low 60,000s in early 2021 to nearly 89,000 by February 2026 — an increase of roughly 45% over five years.

Scale of enforcement: Georgia is issuing and convicting tens of thousands of traffic violations every single month. This demonstrates that law enforcement and courts are actively processing huge volumes of cases.

Relevance to no-insurance: These reports do not break out O.C.G.A. § 40-6-10 (no-insurance) specifically — that’s why DDS redirected you to the counties. However, the sheer volume of convictions shows widespread non-compliance with traffic laws in general. If even a fraction of these involve uninsured drivers, it supports your petition’s core point: the mandatory-insurance requirement is not preventing large numbers of people from driving without coverage.

The county-by-county open records requests we drafted earlier (using the gaclerks.org directory for every county’s clerk email) remain the fastest way to get the actual § 40-6-10 citation counts and fine-revenue numbers.

Looks like smaller counties handle traffic citation revenue through probate magistrate court and charge $1 per page and make you come in and search for specific citations and do not put together reports upon request. Government is not working — these people have AI now

if you live in a small county call the probate court and ask them for revenue from citations of driving without insurance or driving without a license https://georgiaprobatecourt.com/

link to DDS summary statistics illustrating that people are not complying with traffic law generally

[soon.jpg

]

Update from Gwinnett County (one of Georgia’s largest counties): The Recorder’s Court issued ~2,400–2,760 no-insurance citations every year from 2020–2025 and collected $262,000–$315,000 in fines annually.

This is just one county. The mandatory insurance law is not stopping uninsured driving — it is creating a fine-based revenue stream while responsible drivers pay more in premiums. Repeal the mandate and lower costs for law-abiding Georgians.

These charts and numbers come directly from the official Gwinnett County records you received. They are 100% verifiable.

This is why every other county declined to provide me with the requested data for bogus reasons (https://drive.google.com/file/d/121xc6Qoabv0tBQayHNYBTU0Eo4_iBOnw/view?usp=sharing

The mandate is not working: 2,400–2,760 citations every single year in Gwinnett alone. The law has not reduced the problem in six years.

The system profits from failure: The county collected $1.78 million+ in fines while uninsured drivers stayed on the road.

It hurts the compliant: Responsible Georgians pay higher premiums to cover the risk created by thousands of uninsured drivers — while the county pockets the fines.

DDS already admitted the gap: They told you they have no centralized data. Gwinnett’s records show the massive scale at the local level.

DDS Total Traffic Noncompliance and Gwinnette revenue and citations for no insurance. No other county got back to me due to perverse incentives (https://www.dropbox.com/scl/fo/3jybby8tpwwkkoed60fti/ADmlw3o5WBeHdXy9UVmVQ5w?rlkey=ixvepvmjswiq8q2dp5k0amq1u&st=6sj52s0q&dl=0

reddit is a cancer on our democracy and the American mind

Most active Reddit thread here:

https://www.reddit.com/r/GoldandBlack/s/8w8Jp3rf5L

the private roads digression in that thread is concern trolling to derail the topic

lol

final open records request response

43

The Decision Makers

Petition Updates

Share this petition

Petition created on March 19, 2026