Stop Misleading Loans Practices – Demand Transparency and Accountability in Singapore’s

The Issue

73% of SMEs and 1 in 3 Singaporeans have taken a loan at some point. You could have overpaid by thousands without knowing it.

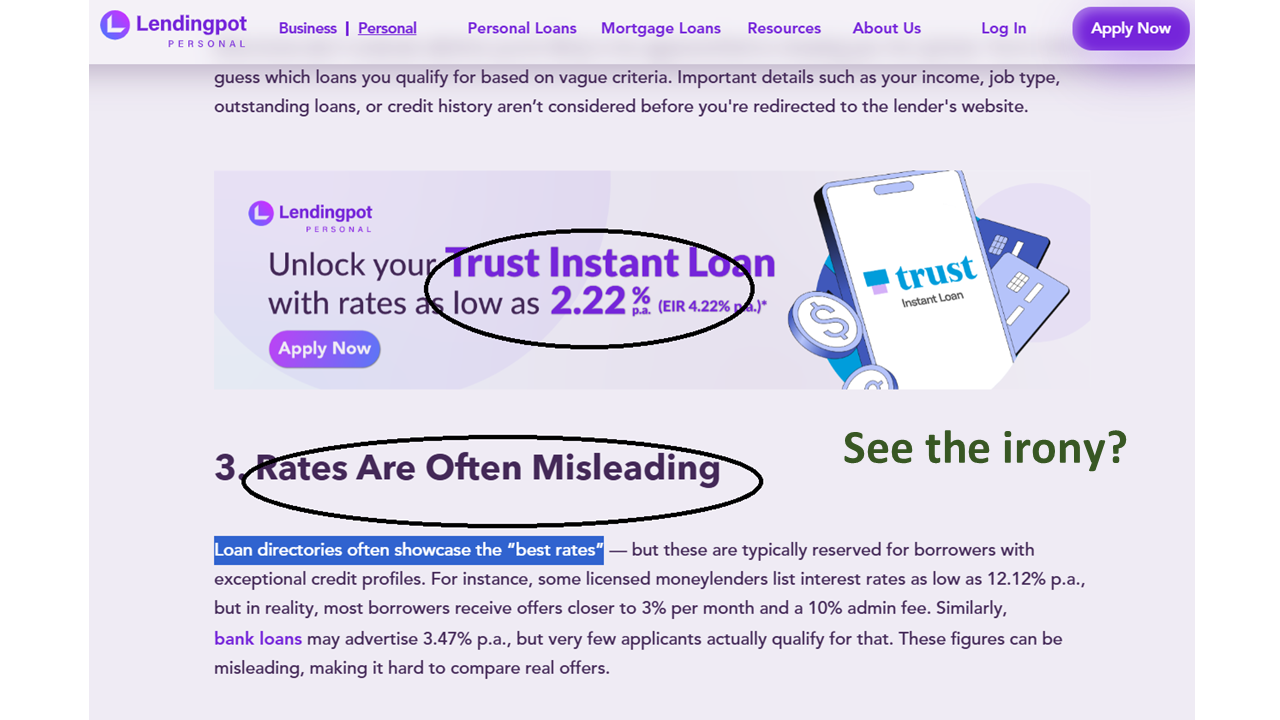

One company even foolishly made their own admission that they are misleading borrowers (we suspect they have been blindly copying our educational materials). They have been running such ads for years, and in "their" article to talk about how comparison websites are misleading, they interestingly showed their very own misleading ads.

Singapore's financial system is known for strong consumer protections, yet loan brokers remain completely unregulated. This leaves borrowers exposed to hidden fees, conflicts of interest, and predatory practices that other advanced economies have long outlawed.

Singapore's Unregulated Loan Broker Industry

In Singapore today—anyone can call themselves a loan broker.

There's no licensing, no required training, no oversight, and no obligation to disclose if there's a conflict of interest, and they can make any false claims. We even have multiple brokers owned directly by lenders.

Unlike tangible services where dissatisfaction is obvious, loan misconduct is harder to detect. If a borrower never knew a lower rate or better terms were possible, how would they know to complain? This information asymmetry allows unethical actors to operate under the radar, leaving victims unaware that they've been exploited at all.

Borrowers may never realize they've overpaid, been misled, or accepted a deal that benefited the broker more than it did them.

The Evidence:

These are some clear lies we found upon some investigation. See if you can spot them:

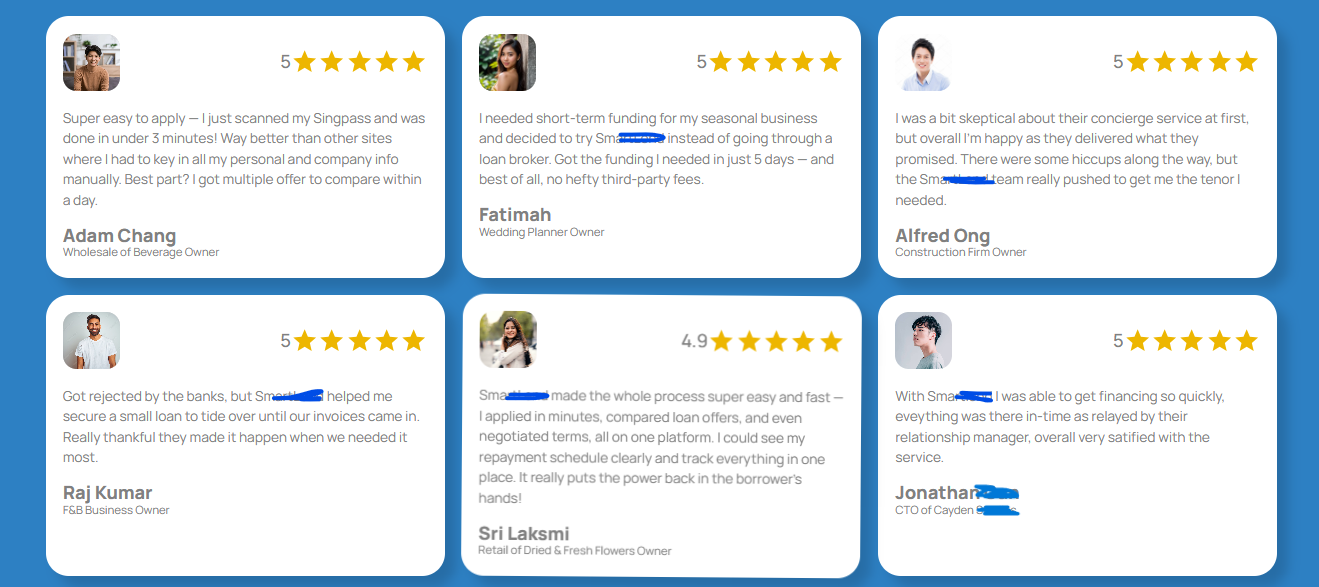

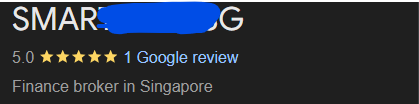

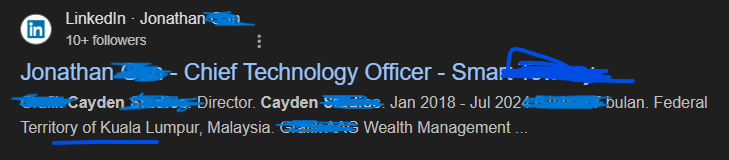

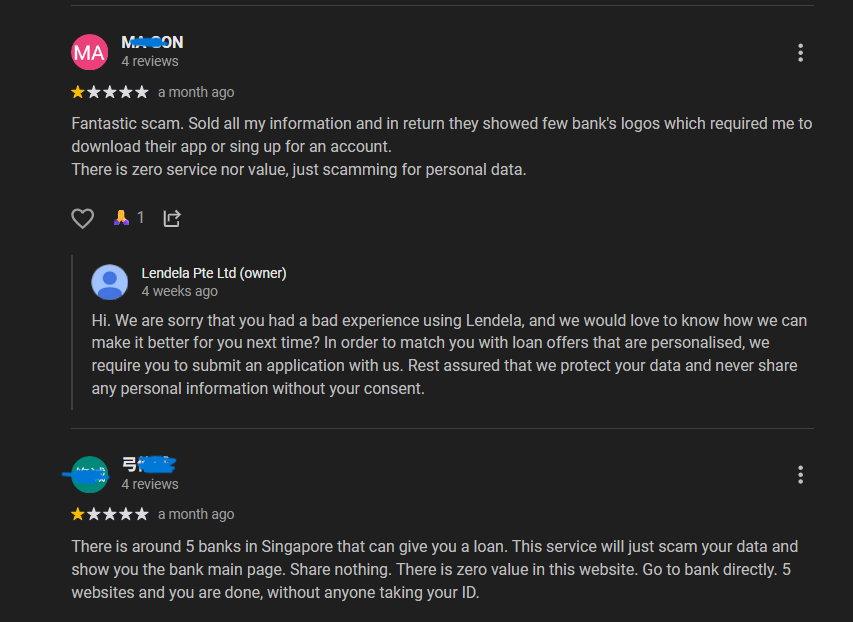

Claim on Google they have 130 5-star reviews, but Google clearly shows one. And so smart, do fake reviews but use staff's names?

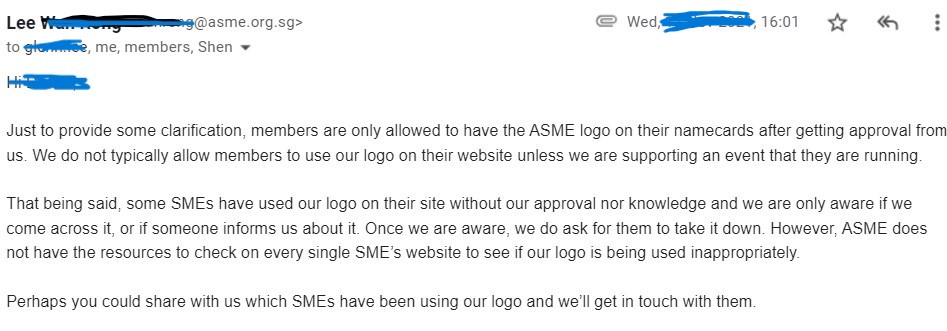

Company names are redacted as of the time for calling them out on social media; we didn't want to directly expose the names.

Run national tv ad to compare online. But was any real offer actually made, or were just some arbitrary offers given?

The Full Scale of Deception

These deceptive loan sales tactics have been exposed in the US and are now reaching our shores. See examples here, here and here.

And that is just the tip of the iceberg. Some other common false claims found on multiple websites include:

-Being able to help the customer get a loan within hours, despite having no control over the lenders that do not work for the brokers.

-Being able to negotiate for better rates when many lenders use machine scoring to make lending decisions and there is no one to even negotiate with

- Claiming to be appointed by chambers

- Fake "As featured As"

- Loan types that doesn't exist

Learn from International Experience: The US Subprime Crisis

Before reforms in the US, mortgage brokers were often incentivized to steer borrowers into higher interest loans, even when they qualified for better terms. These "yield spread premiums" were hidden from consumers and cost them dearly.

Following the 2008 financial crisis, US reforms like the Truth in Lending Act and Dodd-Frank banned broker compensation tied to loan terms and mandated full fee disclosure. Brokers are now required to act in the borrower's best interest.

Yet despite that, in April 2024, a proposed class-action lawsuit alleged that United Wholesale Mortgage worked with brokers to steer borrowers toward costlier loans, resulting in $35 billion in excess fees.

Why Singapore Needs to Act Now

It will be a race to the bottom - as not to be outdone, more and more brokers engage in deceptive claims.

Financial advisors are licensed. Real estate agents are licensed. Why not loan brokers—who influence financial decisions just as serious, for amounts often in the hundreds of thousands to millions?

Unlike motor vehicle dealers caught for odometer tampering or employment agencies charging illegal placement fees—and similar to cases of private schools shutting down overnight or renovation firms disappearing after collecting deposits, which led to the introduction of CaseTrust—loan brokerage misconduct requires proactive regulation, not reactive enforcement.

We call on MAS and Singapore policymakers to:

- Require licensing and training for all loan brokers

- Mandate full disclosure of conflicts of interest

- Ban commission structures that incentivise higher interest rates or hidden costs

- Enforce written KYC and documented recommendations, just like in banking and insurance—so borrowers have proof of what was advised, and brokers can’t make false claims without accountability

- For websites that collect the bare minimum of documents to clearly indicate that they are simplified underwriting and that borrowers may be charged higher interest when that is the case

- Requiring a CaseTrust mark and a vetting process to substantiate their claims on their websites.

#StopClickbait #SGloan

Why Your Signature Matters

While we have written extensively on educating consumers on how things really work, there are many more borrowers we have not reached than we have reached. Borrowers & consumers deserve a system they can trust from the first click and shouldn't need to "study" to know how it works.

It takes you just a few clicks to sign this petition. We hope you can consider doing so.

-----------------------------------

Advocating for greater transparency and accountability in the lending space. To protect borrowers and consumers.

12

The Issue

73% of SMEs and 1 in 3 Singaporeans have taken a loan at some point. You could have overpaid by thousands without knowing it.

One company even foolishly made their own admission that they are misleading borrowers (we suspect they have been blindly copying our educational materials). They have been running such ads for years, and in "their" article to talk about how comparison websites are misleading, they interestingly showed their very own misleading ads.

Singapore's financial system is known for strong consumer protections, yet loan brokers remain completely unregulated. This leaves borrowers exposed to hidden fees, conflicts of interest, and predatory practices that other advanced economies have long outlawed.

Singapore's Unregulated Loan Broker Industry

In Singapore today—anyone can call themselves a loan broker.

There's no licensing, no required training, no oversight, and no obligation to disclose if there's a conflict of interest, and they can make any false claims. We even have multiple brokers owned directly by lenders.

Unlike tangible services where dissatisfaction is obvious, loan misconduct is harder to detect. If a borrower never knew a lower rate or better terms were possible, how would they know to complain? This information asymmetry allows unethical actors to operate under the radar, leaving victims unaware that they've been exploited at all.

Borrowers may never realize they've overpaid, been misled, or accepted a deal that benefited the broker more than it did them.

The Evidence:

These are some clear lies we found upon some investigation. See if you can spot them:

Claim on Google they have 130 5-star reviews, but Google clearly shows one. And so smart, do fake reviews but use staff's names?

Company names are redacted as of the time for calling them out on social media; we didn't want to directly expose the names.

Run national tv ad to compare online. But was any real offer actually made, or were just some arbitrary offers given?

The Full Scale of Deception

These deceptive loan sales tactics have been exposed in the US and are now reaching our shores. See examples here, here and here.

And that is just the tip of the iceberg. Some other common false claims found on multiple websites include:

-Being able to help the customer get a loan within hours, despite having no control over the lenders that do not work for the brokers.

-Being able to negotiate for better rates when many lenders use machine scoring to make lending decisions and there is no one to even negotiate with

- Claiming to be appointed by chambers

- Fake "As featured As"

- Loan types that doesn't exist

Learn from International Experience: The US Subprime Crisis

Before reforms in the US, mortgage brokers were often incentivized to steer borrowers into higher interest loans, even when they qualified for better terms. These "yield spread premiums" were hidden from consumers and cost them dearly.

Following the 2008 financial crisis, US reforms like the Truth in Lending Act and Dodd-Frank banned broker compensation tied to loan terms and mandated full fee disclosure. Brokers are now required to act in the borrower's best interest.

Yet despite that, in April 2024, a proposed class-action lawsuit alleged that United Wholesale Mortgage worked with brokers to steer borrowers toward costlier loans, resulting in $35 billion in excess fees.

Why Singapore Needs to Act Now

It will be a race to the bottom - as not to be outdone, more and more brokers engage in deceptive claims.

Financial advisors are licensed. Real estate agents are licensed. Why not loan brokers—who influence financial decisions just as serious, for amounts often in the hundreds of thousands to millions?

Unlike motor vehicle dealers caught for odometer tampering or employment agencies charging illegal placement fees—and similar to cases of private schools shutting down overnight or renovation firms disappearing after collecting deposits, which led to the introduction of CaseTrust—loan brokerage misconduct requires proactive regulation, not reactive enforcement.

We call on MAS and Singapore policymakers to:

- Require licensing and training for all loan brokers

- Mandate full disclosure of conflicts of interest

- Ban commission structures that incentivise higher interest rates or hidden costs

- Enforce written KYC and documented recommendations, just like in banking and insurance—so borrowers have proof of what was advised, and brokers can’t make false claims without accountability

- For websites that collect the bare minimum of documents to clearly indicate that they are simplified underwriting and that borrowers may be charged higher interest when that is the case

- Requiring a CaseTrust mark and a vetting process to substantiate their claims on their websites.

#StopClickbait #SGloan

Why Your Signature Matters

While we have written extensively on educating consumers on how things really work, there are many more borrowers we have not reached than we have reached. Borrowers & consumers deserve a system they can trust from the first click and shouldn't need to "study" to know how it works.

It takes you just a few clicks to sign this petition. We hope you can consider doing so.

-----------------------------------

Advocating for greater transparency and accountability in the lending space. To protect borrowers and consumers.

The Decision Makers

Petition Updates

Share this petition

Petition created on 16 July 2025